The results of the latest business rates revaluation reveal a growing divergence in property prices between London and the rest of the country. Increases in the value of non-residential property in the capital are set to raise rates bills by 11%, on average, increasing the tax take by over £700 million. This will be offset by reductions in bills and revenues in most of the rest of England, and especially the North, as property values fall behind. Growing differences in property prices reflects broader evidence of a growing divergence in economic performance over the last few years. And it will contribute to the ongoing trend of the UK government becoming more and more dependent on revenue from London to fund services across the whole – which may pose difficulties if more revenue sources are devolved to the local level. This observation discusses this and other issues related to today’s revaluation figures.

Background

Business rates – a tax paid by businesses and other occupiers of non-residential property and based on the value of that property – are a big deal: across the country as a whole they are forecast to raise £28.4 billion in 2016–17. This is almost as much as is forecast to be raised from council tax (£31.4 billion)– a tax levied on residential property, which in aggregate is worth around 4-5 times as much as non-residential property.

At the moment, business rates are assessed on 2008 property values. Today, the Valuation Office Agency has announced the updated 2015 property values that will be used to calculate business rates from April 2017. This is also a big deal: between 2008 and 2015 property values have changed very differently in different parts of the country, with very large increases in some areas (notably ‘gentrifying’ parts of London), and big decreases in others (such as ‘struggling’ town centres in much of the rest of the country). These relative changes will have a huge effect on business rates bills.

The business rates system works in a slightly odd way. The tax bill is calculated as the value of a property multiplied by a tax rate (called ‘the multiplier’). The multiplier generally increases in line with inflation in the years between valuations such that revenues also rise roughly in line with inflation (although in 2014 and 2015 the government capped the increase at 2%).

Perhaps surprisingly, across England as a whole, the value of non-domestic property is estimated to have risen by around 11%, on average, between 2008 and 2015. If the same multiplier (i.e. tax rate) were kept, revaluation would therefore lead to overall business rates revenues rising. To stop this happening, the multiplier would have to be reduced by 11% to ensure that average bills do not increase simply as a result of the revaluation.

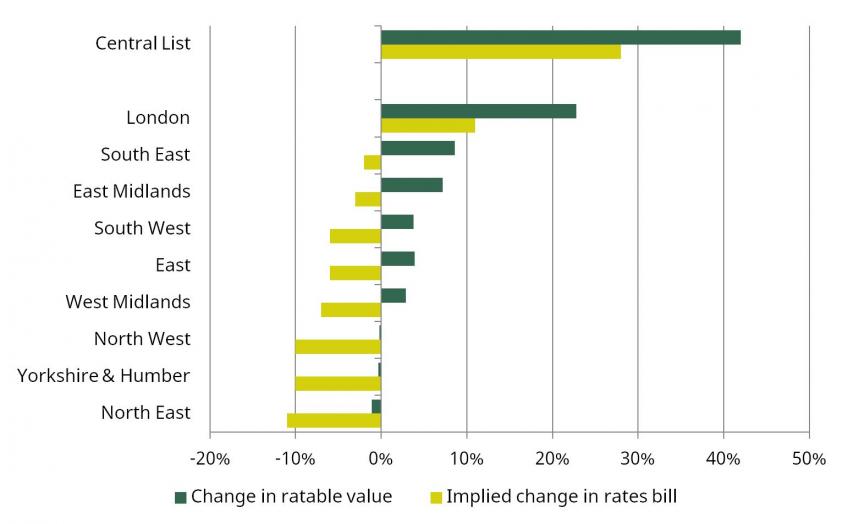

The impact of revaluation on rates bills across England

Rateable values – and hence rates bills – are changing differently for different properties and different parts of England. The figure below show the average estimated change in rateable value and the implied change in business rates bills as a result of the revaluation for the different regions in England, as well as the so-called ‘central rating list’ (which includes things like transport, energy, water, and telecoms infrastructure that are often national in scope, and therefore are not allocated to any particular council or indeed regions).

Figure 1. Average change in rates bills due to revaluation, by region, before accounting for adjustment to multiplier to account for expected appeals

Source: CLG Business Rates Revaluation Consultation and VOA rateable value data.

It shows bills falling by 10% or more, on average, in the northern regions of England, but increasing by 11% in London, on average. Such changes would mean that in today’s terms, more than £700 million more business rates revenues would eventually be raised in London and around £1.2 billion less in the other regions of England (with an increase in revenues from the central list making up the missing £500 million or so).

The fact that London’s rates bills will be rising reflects its non-residential property market outperforming that in the rest of England – presumably because London is an increasingly relatively more attractive place to set up shop (or office). The same pattern of London economically outperforming the rest of the country, and especially the north, can be seen in many other indicators. Gross value added increased around three times as fast in real terms in London as in the rest of England between 2008 and 2014, for instance. The numbers of people in employment has grown by 15% in London since 2008, compared to 4% in the rest of England. And of course, residential property prices have risen far beyond their pre-Credit Crunch peak in London, but still lag in much of the North.

This trend means the UK government is becoming more and more dependent on revenues – from many other taxes like income tax, as well as business rates – from London to fund services across the country as a whole. At the same time there is growing pressure for devolution of more of London’s revenues to the Greater London Authority – a difficult square to circle if these trends continue.

The impact on individual businesses

The impact of revaluation on individual properties’ business rates bills can be much larger than the impact on average regional bills. For instance, 242,000 small properties – those with a value less than £28,000 in London and £20,000 outside London – are estimated to see their rateable value rise to such an extent as to imply increases in their bills of at least 24%. On the other hand, 141,000 would be due cuts of more than 20%.

To ease the pain of business rates increases for those seeing the biggest increases, it has become customary to offer ‘transitional protection’ – funded by slowing the ‘gain’ from those benefitting from cuts to their business rates. The government is currently consulting on the details of the scheme this time round but its preferred scheme would apply to almost half of properties in 2017–18 and almost 5% even after five years in 2021–22: a long transition. There is clearly a trade-off between offering such protection and ensuring business rates respond fully to the changing reality of local property markets and economies. If there are worries about big changes in bills at revaluation, a better solution would probably be to revalue more frequently – e.g. every 2 or 3 years –, because the changes in relative values should be smaller over these shorter time periods.

The way the transitional protection system is set up also, in effect, redistributes from large properties (where increases in bills are capped at relatively high levels, and cuts at relatively low levels) to small properties (where the opposite is true). For instance, the government estimates only 8,800 large properties will be benefitting from transitional protection in 2017–18; but 9,700 will still be paying for transitional protection even in 2021–22.

Will I pay more next year?

The rates bills people will actually pay from next April will be affected by two other factors though. First, if history is a guide, many ratepayers will successfully appeal against their new values and get cuts in their rateable values and bills. To recoup these expected losses, the government will make an upwards adjustment to the multiplier, pushing up all rates bills. Second, as is usually the case, the multiplier is set to increase in line with September 2016 RPI inflation, forecast to be 1.7%.

After accounting for these factors as well, the government estimates the standard multiplier will be 0.48 next year, around 3% lower than the current 0.497. This means that properties that have seen their rateable value increase by around 3% or less can expect a cut in their rates bill next year, while those whose value has increased by more than 3% can expect an increase in their bill next year.

The impact on councils

Finally, it’s worth considering the impact on those who collect business rates – councils. Initially, the revenues of individual councils won’t change as the result of the revaluation (the government will redistribute funding between different councils to ensure no council wins or loses overnight). But, there may still be winners and losers in subsequent years. First, because councils in England notionally keep 50% of any change in their business rates revenues, any subsequent growth (or decline) in the business rates tax base will be worth more in those areas where rateable values have increased by more than average – and hence rates bills will increase –, and vice versa. Second, councils will have to bear their share of any successful appeals against the new values – and while estimates of the impact of such appeals can be made when the new valuations are introduced, such estimates are unlikely to be completely accurate.

The revaluation proceeds even bigger changes to the way business rates fit into the local government finance system. April 2017 will also see Liverpool and Manchester become pilots for a 100% business rates retention system that is set to roll out across England by 2019–20. This will have a big impact on the kinds of financial risks and incentives councils face. The IFS is launching a major research programme to look at these and other issues related to local government and devolution. Our first report, setting out the context and key issues, will be published on 26th October.

This analysis is part of a project funded by the Local Government Finance and Devolution Consortium. Members of the consortium include Capita, CIPFA, PwC, the Municipal Journal and the Society of County Treasurers.

Notes on sources

Information on rateable values is available from the Valuation Office Agency (see https://www.gov.uk/government/statistics/non-domestic-rating-high-level-estimates-of-change-in-rateable-value-of-rating-lists for regional summaries). Information on the implied changes in bills and transitional protection is available from the Department for Communities and Local Government (https://www.gov.uk/government/consultations/business-rates-revaluation-2017).

Statistics on GVA (http://www.ons.gov.uk/file?uri=/economy/grossvalueaddedgva/datasets/regionalgrossvalueaddedincomeapproach/current/gvaireferencetables.xls) and employment (https://www.ons.gov.uk/releases/regionallabourmarketstatisticsintheuksep2016)are available from the Office for National Statistics. House Prices are available from the Land Registry (http://landregistry.data.gov.uk/app/ukhpi/explore).

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research