The overall funding settlement for schools will feel quite different over the next five years compared with the previous five.

Under the coalition government, school spending in England was relatively protected at a time when other areas of government saw large cuts, with many unprotected departments seeing their non-investment budgets cut by 20% or more between 2010–11 and 2014–15. Current or day-to-day spending on schools grew by 3% in real terms between 2010–11 and 2014–15. Even after allowing for the growth in pupil numbers over this period, spending per pupil still rose by 0.6% in real terms.

The picture for day-to-day spending on schools contrasts with other areas of education spending that saw larger cuts: 16–19 education spending fell by 14% in real terms over the last parliament and education capital spending fell by 34% in real-terms.

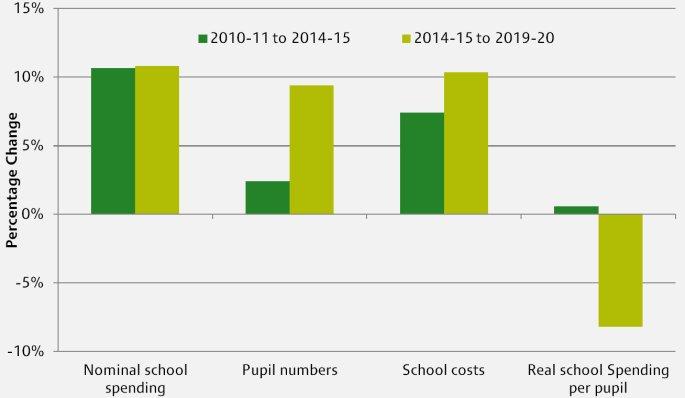

The new Conservative government has also offered schools in England considerable protection, committing to protecting day-to-day spending per pupil in cash terms over the current parliament. As shown in the figure below, this will actually mean a similar rate of growth in nominal spending as seen in the last parliament. However, increasing costs and increasing pupil numbers mean that resources per pupil are likely to fall significantly.

Our research at the Institute for Fiscal Studies (IFS), funded by the Nuffield Foundation, shows that key cost increases include the average public sector pay settlement of 1% per year announced in the Summer Budget. In addition schools will see an increased employer National Insurance Contributions bill from April 2016 as the reduced rate associated with contracting out will cease. This comes on top of the increase in employer pension contributions to the teachers’ pension scheme that came into force in April 2015.

Taking these together with pressures on other costs, we forecast that school spending per pupil is likely to fall by around 8% in real terms (based on a school specific measure of inflation) between 2014–15 and 2019–20. This is actually a less severe squeeze than looked likely at the time of the election (when we thought it would be around a 12% cut per pupil). But that only reflects the tighter 1% pay increase announced in the Budget. That will ease the pressure on schools costs, but might make recruitment and retention of teachers and other staff more difficult.

Even so, this will be the first time since the mid-1990s that school spending has fallen in real terms (when spending per pupil fell by 3.6% in real terms between 1993 and 1997).

Figure: Percentage Changes in School Spending and Cost Factors, 2010-11 to 2019-20

Sources and Notes: Figures for nominal school spending taken from http://election2015.ifs.org.uk/article/schools-spending; Pupil Numbers taken from https://www.gov.uk/government/statistics/national-pupil-projections-trends-in-pupil-numbers-july-2014; methodology for calculating school costs for 2014–15 to 2019–20 can be found in http://election2015.ifs.org.uk/article/schools-spending; Growth in paybill per head figures are not available before 2014–15 and we therefore assume school costs follow the growth in the GDP deflator of 7.4% between 2010–11 and 2014–15, which is likely to slightly over-state cost increases for schools given that average weekly earnings for public sector workers only increased by 5.5% between 2010–11 and 2014–15.

Challenges ahead

A significant challenge on the teacher workforce over the next five years will be recruiting the required number of teachers, and of sufficient quality and motivation, at a time of continued public pay restraint and rising pupil numbers.

The pupil population is currently expected to rise by 450,000 from 6.45 million in 2016 to 6.9 million in 2020. If there was a desire to keep the pupil:teacher ratio constant, the number of teachers would need to increase by 30,000 (from 450,000 today to 480,000 by 2020). Although not without precedent (a similar increase occurred in the early 2000s), it could prove difficult to increase teacher numbers at a time when public sector pay seems likely to fall relative to that in the private sector. Alternatively, schools and policymakers could allow the pupil:teacher ratio to rise, implying potentially larger class sizes.

The government has also signalled its intention to reform the school funding system to ensure (sensibly) that areas with similar populations receive the same level of funding per pupil. Although it made some tweaks at the end of the last parliament, this only went some way to address the problem that similar areas can receive quite different levels of funding per pupil. However, substantial reform will be particularly difficult for policymakers to implement when overall school spending per pupil will be frozen in cash-terms. Delivering a cash-terms increase to some schools or local authorities as a part of a set of reforms would require cash-terms cuts to some other groups of schools or local authorities. Schools do have some experience of receiving overall cash-terms cuts when pupil numbers fall. However, delivering cash-terms cuts in funding per pupil could be a lot more challenging.

Summary

Schools in England experienced a relatively benign scenario under the last parliament at least relative to many other public services. But this is now set to change. We forecast they will see an overall cut of 8% per pupil in real terms over the next five years. This will be a new experience for many in the school sector – the last real-terms cuts were in the mid-1990s – and will make issues around teacher recruitment and reform of the school funding system more difficult.

However, it is important to remember that schools are still relatively protected compared with many other areas of government and other areas of education spending. Further education and sixth form spending fell by 14% in real terms under the last parliament and could experience even larger cuts under this parliament. Unprotected government departments are currently expected to see their spending fall by 27% in real-terms between 2015–16 and 2019–20.

Authors

Luke Sibieta

Luke is a Research Fellow at the IFS and his general research interests include education policy, political economy and poverty and inequality.

Chris Belfield

More from IFS

Understand this issue

Policy analysis

Academic research