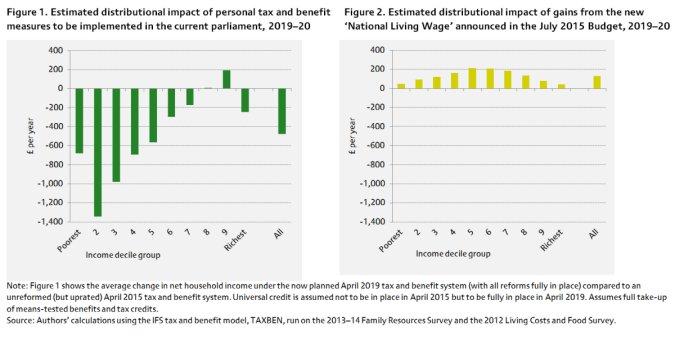

A number of changes to the tax and benefit system have been announced for implementation in the current parliament as part of the government’s deficit reduction programme. An analysis by researchers at the Institute for Fiscal Studies (IFS) finds that the package of changes to tax, tax credits and benefits will reduce household incomes significantly, particularly for those towards the bottom of the income distribution.

The July 2015 Budget also announced a substantial increase in the national minimum wage for those aged 25 and over, which the Chancellor described as a new “National Living Wage” (NLW).

New analysis by IFS economists, published in an IFS Briefing Note, analyses the extent to which the new NLW will compensate for the losses caused by the tax and benefit reforms for different types of households in 2019–20.

Among households with someone in paid work, those eligible for benefits and tax credits are estimated to lose an average of £750 per year from the changes to tax and benefits. On the other hand, the average gain from the new NLW for this group of 8.4 million working-age households is estimated to be £200 per year. This suggests that the new NLW will, on average, compensate for 26% of the losses this group of working households will see from changes to taxes, tax credits and benefits. They will remain £550 worse off per year, on average.

Households where no one is working – who are estimated to be hit especially hard by the tax and benefit changes – cannot gain from the new NLW.

Our scenario suggests that only around 13% (£150 per year) of the losses due to tax and benefit changes (£1,090 per year) of all working age households currently entitled to benefits and tax credits – including non-working households – will be offset by the NLW, on average.

These estimates assume that the new NLW will have no effect on GDP, employment or hours of work. In fact, as the Office for Budget Responsibility stresses, the new NLW is likely to depress GDP and employment, and the money for higher wages has to come from somewhere. In part because of this, these estimates are likely to represent a “better case” scenario for the impact of the NLW on household incomes.

The new NLW offers such little compensation because the boost to gross wages is smaller than the announced fiscal tightening, and almost one-third of the increase in gross wages goes to the Treasury in higher tax receipts and lower benefits and tax-credit entitlements.

The Briefing Note finds that the households gaining from the new NLW are often not the households losing the most from the tax and benefit reforms announced. It is households in the lower half of the income distribution who stand to lose the most from the reforms to taxes and benefits. The households gaining from the new NLW are more evenly distributed across the income distribution, with the largest gains in the middle.

The average losses from tax and benefit changes in deciles 2, 3 and 4 of the household income distribution are £1,340, £980 and £690 per year, respectively. These same groups are estimated to gain £90, £120 and £160 from the new NLW (again in a “better case” scenario). This suggests that a “better case” estimate of the compensation the new NLW offers these groups on average is 7%, 13% and 24%, respectively.

William Elming, a research economist at the IFS and co-author of the briefing note said: “The new ‘National Living Wage’ will only offer partial compensation to working age households who will see their incomes fall as a result of tax and benefit changes announced for the current parliament. There may be strong arguments for introducing the new NLW, such as increasing earnings and the incentives to work for the low paid. However, the new NLW cannot be considered a direct substitute for benefits and tax credits aimed at lower income households. The wage increases are not as large as the benefit cuts. And, it is not targeted at the same group who lose from the cuts.”

Notes to editors

1. The IFS Briefing Note entitled “An assessment of the potential compensation provided by the new ‘National Living Wage’ for the personal tax and benefit measures announced for implementation in the current parliament” by William Elming, Carl Emmerson, Paul Johnson and David Phillips is available on the IFS website: http://www.ifs.org.uk/publications/7975

2. The Briefing Note was prepared for the House of Commons Treasury Select Committee and has been published on the committee’s website.

3. The authors gratefully acknowledge funding from the Economic and Social Research Council via the Centre for the Microeconomic Analysis of Public Policy.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Paul Johnson

Paul has been the Director of the IFS since 2011. He is also currently visiting professor in the Department of Economics at University College London.

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

William Elming

More from IFS

Understand this issue

Policy analysis

Academic research