Costas is a Research Fellow of the Institute. He is also Professor of Economics at Yale University and Visiting Professor at University College London. His research interests are Econometrics, Public policy, Labor economics, Economics of education, Microeconometrics, Evaluation of public policy, Household behavior, Retirement and pensions, Income distribution, Consumption, Demand analysis, Investment and Development economics.

Education

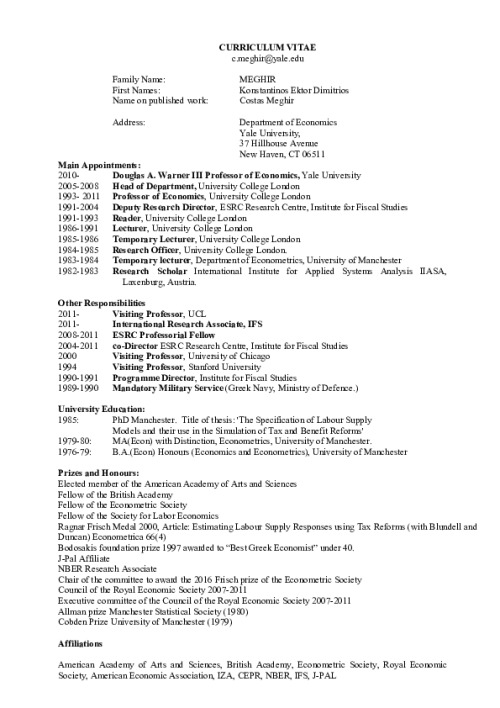

PhD Economics, University of Manchester, 1985

MA (with Distinction) Economics, University of Manchester, 1980

BA (1st Class Honours) Economics and Econometrics, University of Manchester, 1979

This paper investigates the impact of pupil-teacher ratios on later life earnings. We find no impact on the earnings of men, but a lower pupil-teacher ratio does increase the earnings of women – particularly low ability women.

This paper uses microeconomic data from the U.K. Family Expenditure Surveys (FES) and the General Household Surveys (GHS) to describe and explain changes in the distribution of male wages.

We explore the role that economic incentives, particularly changes in wages at the bottom end of the wage distribution, play in determining crime rates.

This paper provides a non-technical review of the evidence on the returns to education and training for the individual, the firm and the economy at large

In this article we argue that the life-cycle model that allows demographics to affect household preferences and relaxes the assumption of certainty equivalence can generate hump-shaped consumption profiles over age that are very similar to those observed in household-level data sources.

This paper uses microeconomic data from the UK Family Expenditure Surveys (FES) and the General Household Surveys (GHS) to describe and explain changes in the distribution of male wages.

Moment conditions are derived for dynamic linear panel data models with linear individual specific effects in the mean and multiplicative individual effects in the conditional ARCH type variance function.

The authors propose a method to test for liquidity constraints which relies on using the within period marginal rate of substitution condition as a benchmark to evaluate the intertemporal Euler equation.