Downloads

BN211.pdf

PDF | 796.42 KB

Higher education (HE) in England has been subject to near-constant reform over the past two decades. The most notable of these was the 2012 trebling of tuition fees to £9,000. HE is an area where England is a genuine world leader having long boasted several of the world’s finest universities, yet that position is increasingly under threat from increased global competition. Understanding the impact of various reforms on government, universities and students is therefore crucial.

Previous IFS research has evaluated the 2012 reform, finding that it increased overall graduate contributions considerably but actually reduced lifetime repayments for those in the bottom third of the graduate lifetime earnings distribution.

In this briefing note we use the IFS HE finance model to provide up-to-date estimates of the long-run cost of undergraduate loans to the government taking into account these recent changes. We consider the impact of the 2012 reform and the changes since 2012 separately by estimating the long-run government loan subsidy (the ‘RAB charge’) and the overall long-run cost to government for the 2017 cohort of students under three different HE finance systems (the ‘2011 system’, the ‘2012 system’ and the ‘2017 system’).

We also consider the system from the point of view of students, showing debt on graduation, ‘cash-in-pockets’ for students at university, and graduates’ lifetime loan repayments. We highlight the role of recent reforms, further freezes to the thresholds at which loan repayments are made, and the use of the positive real interest rates. To complete the picture for the changes since 2011, we focus on the status of university finances, highlighting the impact of recent reforms on the relative incentives to provide courses in different subjects. Finally, we consider some policy options, qualitatively outlining the potential impact of various reforms on the system of HE finance in England.

Key findings

| There has been a big shift in the way government funds higher education (HE) from up-front grants to student loans. | Tuition fees were introduced in 1998, and increased in 2006 and again in 2012. This has increased overall funding, but teaching grants have declined. Maintenance grants have also been scrapped. Consequently, 96% of up-front government support is now in the form of loans. | |

| This has dramatically reduced deficit spending, while also reducing the expected long-run taxpayer contribution. | A key factor is that loans do not count towards the deficit, while grants do. Since 2011, the contribution of HE spending to the deficit has declined by £5.7 billion (around 10% of the current deficit), while university funding has increased. The long-run taxpayer contribution has decreased by less – around £3.1 billion – because graduate contributions have increased, but by less than the increase in the loans provided. | |

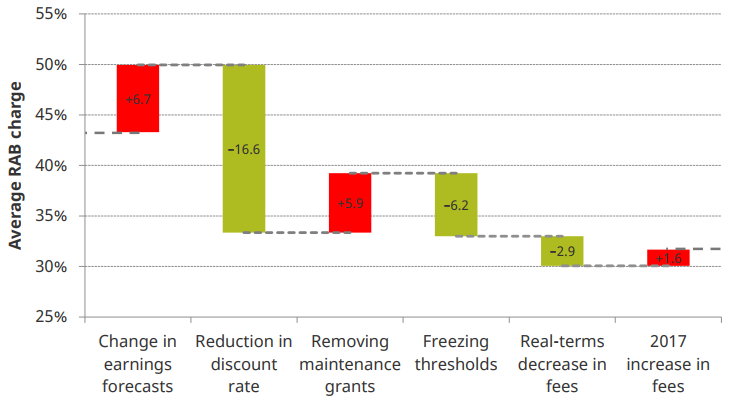

| The long-run taxpayer contribution has become considerably more uncertain. | The long-run contribution is now heavily dependent on graduate earnings, early repayment behaviour and the government cost of borrowing; for example, if graduate earnings are 2 percentage points lower than expected, the long-run government contribution increases by 50%. | |

| Students now graduate with average debts of £50,000 – and even more for the poorest students. | The combination of high fees and large maintenance loans contributes to English graduates having the highest student debts in the developed world. The 2015 policy that replaced maintenance grants with loans means students from the poorest backgrounds will accrue debts of £57,000 (including interest) from a three-year degree. Their ‘cash in pockets’ has been protected, but now it is almost entirely in loans rather than free cash. | |

| Student loans differ from private loans, as repayments are proportionate to income. | Consequently, there is significant variation in graduate contributions, with the highest earners repaying considerably more than the lowest. However, changes since 2012 have increased the repayments of almost all graduates, increasing the burden of student loans the most for low and middle earners – driven largely by the freezing of the repayment threshold. | |

| Positive real interest rates increase debt levels for everybody – but only the repayments of the highest earners. | The use of RPI + 3% during study – currently 4.6% nominal, but rising to 6.1% in September – results in students accruing £5,800 in interest on average during study. Positive rates do not affect the loan repayments of those below the median, as they do not repay their principal. However, for high earners, the use of RPI + 0–3% rather than CPI + 0% increases lifetime repayments by almost £40,000 in today’s money. This is due to lengthening the period of repayment rather than increased payments in any given year. | |

| The benefits from high interest rates appear to outweigh the costs. | There is a risk that better-off parents will pay fees up front, especially if they think their offspring will be high earners. This would increase the cost to government in the long run, as high-earning graduates repay more than the value of their loans. However, even if all of the top 20% do not take out loans, the increased cost is outweighed by the significant revenue forecast to be generated by the positive real rates. | |

| Recent reforms have considerably changed the landscape for UK universities. | The 2012 reform increased average university funding by 25%. It also considerably changed the relative per-student income of providing different courses; for example, funding for ‘Group A’ (high-cost) courses increased by only 6% between 2011 and 2017, while ‘Group D’ (low-cost) funding increased by 47%. This may affect universities’ incentives. | |

| Cutting fees while protecting university funding would increase the deficit and the long-run taxpayer contribution, but would also increase flexibility. | Large fee cuts would reverse recent changes and increase both deficit spending and the long-run taxpayer contribution to HE. However, unlike the current system, under which the vast majority of the taxpayer contribution comes through the unpaid loans of low earners, replacing the lost fee income by teaching grants would allow government to target high-priority subjects (such as STEM-based courses) or students (such as those from low-income households). |

Figure 2.1. Impact of sucessive changes on RAB charge

Authors

Lorraine Dearden

Jack Britton

Jack's main interests lie in human capital accumulation and discrete choice dynamic modelling.

Chris Belfield

Laura van der Erve

More from IFS

Understand this issue

Policy analysis

Academic research