From tomorrow, Scottish residents will for the first time be subject to a different income tax schedule from those resident elsewhere in the UK. This is because of the Scottish parliament’s decision to use recently devolved powers over income tax bands and rates for non-savings and non-dividend income to freeze the higher-rate threshold (the point at which the rate of income tax rises from 20% to 40%) for the new financial year.

By default, the higher-rate threshold would rise from its current level of £43,000 to £43,900 in 2017–18 both in and outside Scotland (given standard inflation uprating and UK-wide changes to the personal allowance). Instead, the UK parliament has decided to increase this to £45,000, reducing taxes for 4.4 million people at a cost of around £600 million per year, while the Scottish parliament has decided to hold this fixed at £43,000, increasing taxes for around 350,000 of Scotland’s 2.5 million income taxpayers, raising around £60 million per year. While initially relatively small – the maximum tax rise in 2017-18 is £180 per year –, this difference looks set to at least double over the coming years; a result of the Conservative Party manifesto promise to raise the higher-rate threshold to £50,000 by the end of the parliament, and the Scottish government’s stated intention to increase it by at most inflation over the same period (implying a Scottish higher-rate threshold of at most £46,000 by 2020–21 given current forecasts).

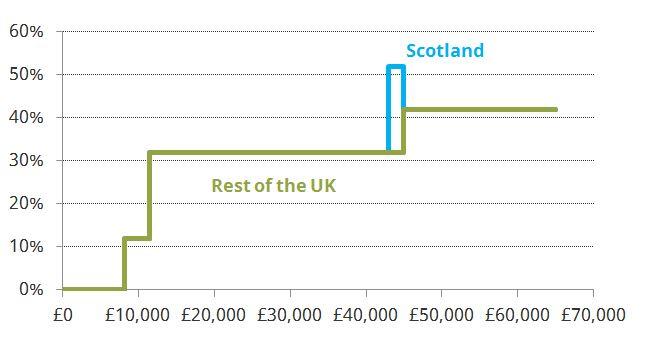

The Scottish parliament now has significant power to set the rates and thresholds of income tax that apply to the earnings of Scottish residents, but it has no such control over the taxation of savings and dividend income or National Insurance contributions (NICs). One consequence of this is that the earnings of Scottish residents will be subject to a peculiar tax schedule, shown in the Figure below, with a combined rate of income tax and employee NICs that rises from 32% to 52% at £43,000 per year, before falling back to 42% at £45,000.

Combined income tax and employee NICs schedule, 2017–18

Note: assumes standard personal allowance and all income from earnings which are constant through the year.

This is because employee NICs are levied at a rate of 12% up to a threshold known as the Upper Earnings Limit (UEL), and 2% above. The UK government has decided to keep this aligned with the income tax higher-rate threshold that applies outside of Scotland: as the Figure shows this means that employees with straightforward tax affairs outside Scotland will pay income tax and employee NICs at a combined rate of either 12, 32, or 42%, compared to the more complicated schedule facing those in Scotland.

Scotland’s newly craggy rate schedule should serve to remind that retaining separate systems of income tax and NICs creates substantial complexity in the overall system of earnings taxation. In fact, these parallel systems can already create incoherent rate schedules of the kind depicted in the Figure above for those whose earnings fluctuate through the financial year, simply because income tax is assessed against annual income whereas NICs is assessed within each pay period. Complexity of this kind looks especially needless given that NICs are now essentially just another income tax levied on earnings, with virtually no link remaining between the NICs someone pays and the benefit entitlement they accrue. There is therefore a strong case for merging the two taxes, as set out in the IFS-led Mirrlees Review.

In the absence of such moves towards integration on a UK-wide basis, devolving NICs would allow the Scottish parliament to limit the additional cragginess in the tax schedule that arises from not following Conservative Party plans to raise the UEL and higher-rate threshold in the rest of the UK. As previously argued by IFS researchers, the ability to set NICs rates and thresholds would be a logical counterpart to those powers already granted over non-savings and non-dividend income tax, if devolution of further tax revenues to Scotland were seen as desirable.

Decisions by the Scottish parliament to set income tax rates or thresholds that differ from those elsewhere in the UK will also have implications for the incentive to carry out similar work through different legal forms. This is because Scottish company owner-managers can take income in the form of dividends which are taxed less heavily than the incomes of either the self-employed or employees, at rates and bands determined by the UK parliament. By setting the higher-rate threshold for earned income below that set in Westminster for dividend income, the Scottish parliament exacerbates this existing tax incentive to carry out economic activity in Scotland through corporate form.

As well as distorting the decisions individuals make about how to work, deviating from the UK government’s income tax policy can have implications for the Scottish budget beyond the revenue directly raised or foregone. For example, under the current fiscal framework, were incorporation to rise faster in Scotland than elsewhere in the UK – as it might in response to a larger tax differential – Scottish revenues would fall without any offsetting block grant adjustment.

These issues highlight just some of the complexities that will arise as the Scottish parliament makes use of its substantial new powers of taxation. But they are also a useful illustration of some of the more fundamental deficiencies that continue to afflict the tax system throughout the UK, and remain in need of reform.

Authors

Barra Roantree

Barra is a Research Fellow at IFS and Assistant Professor of Economics at Trinity College Dublin.

More from IFS

Understand this issue

Policy analysis

Academic research