Productivity is currently the most talked about topic in town, and for good reason. At the end of 2014, UK productivity remained below its pre-recession level and 16% below where it would have been had the pre-recession trend continued. Looking forward, it is only productivity growth that is likely to spur increases in real wage growth and living standards. Alongside the upcoming budget, George Osborne will set out a plan for how to boost productivity.

This Observation aims to provide some context for current discussions by setting out what the most recent data shows about the trajectory of productivity across different sectors of the economy.

Productivity trends by industry

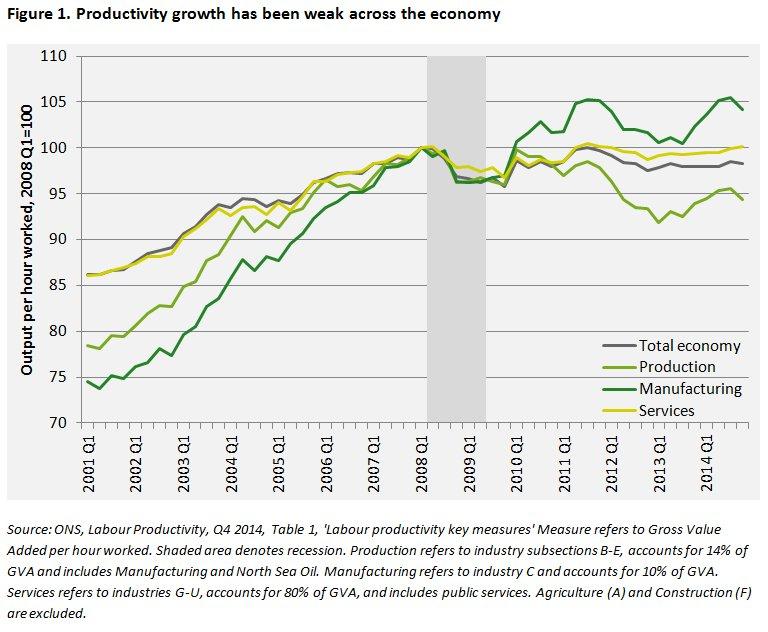

Figure 1 shows how total productivity – output per hour worked – fell at the start of the recession and recovered up to 2011. A similar pattern was observed in both manufacturing and service industries. Across the economy, productivity actually fell through 2011. Since then, manufacturing industries have regained some of their lost ground, but service sector productivity has been stagnant over the past three years. A large part of what explains the trend in the production sector is the ongoing decline in North Sea oil production, which accounts for around 1.4% of the economy and is likely to see a permanently reduced rate of productivity growth. While there are differences between sectors, it is clear that none is close to where they would have been had the pre-recession trend continued.

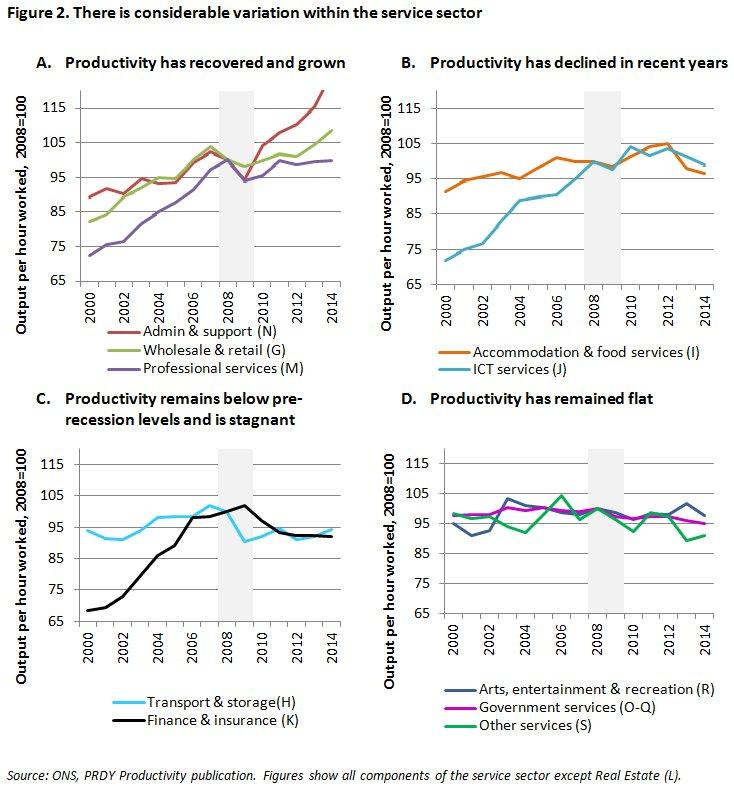

The service sector accounts for close to 80% of output and is therefore the most important driver of economy-wide productivity growth. Within the stagnant productivity performance of the sector as a whole there is considerable variation, with some sub-sectors quickly returning to pre-recession growth levels and others remaining well below pre-recession levels.

The relatively good news stories are administrative and support services, wholesale and retail and professional services (Panel A). These sectors, which together account for approximately 25% of output, saw strong productivity growth before the recession and have recovered to their pre-recession levels. Administrative and support services and wholesale and retail trade are now seeing productivity growth rates above the average pre-recession trend, while professional services has seen little growth in productivity since 2011.

Accommodation and food services and ICT services were sectors with productivity growth before and immediately following the recession (Panel B). Yet in the last two years productivity has been in decline. These sectors account for around 9% of output.

Transport and storage and finance and insurance together make up around 12% of output and are notable as examples where productivity is still substantially below the pre-recession level and has shown little sign of recovery. It is often highlighted that the financial industry was important for UK productivity growth before the recession and that going forward productivity growth may be permanently reduced. However, as these figures show, weak productivity growth is a feature of much of the service sector. Even if productivity in financial services had continued on its very strong pre-recession trend, overall productivity levels would still only be 2.3% above their 2008 level, and still 11% below where it would have been had the overall pre-recession trend continued. The slowdown in productivity growth in financial services is therefore only part of the explanation for recent trends.

Finally, there are some industries that did not see growth either before or after the recession. These include government services (19% of output). As such, the weak performance in these industries does not explain why overall service sector productivity growth is so much lower than before the crisis.

Summary

Productivity growth has been weak in almost all sectors of the economy, and negative in some. The lack of productivity growth in the finance sector has been important, but cannot explain the majority of the recent weakness.

Much has been written about the various explanations for the lack of productivity growth, which include low investment in new capital, an impaired allocation of resources, higher employment as a result of weak wages and possibly some measurement error. When the Chancellor sets out his productivity plan, the focus is likely to be on those areas of public policy that we can be confident matter for productivity, such as investment in skills, science and infrastructure. Such investments could provide a welcome boost to productivity in the medium term but are unlikely to provide immediate fixes for current productivity. Finding ways to boost productivity today will be much harder.

Authors

Rachel Griffith

Rachel is Research Director and Professor at the University of Manchester. She was made a Dame for services to economic policy and education in 2021.

Helen Miller

Helen is Deputy Director of the IFS and Head of the Tax sector.

More from IFS

Understand this issue

Policy analysis

Academic research