Downloads

wp1024.pdf

PDF | 1.53 MB

Governments wishing to reduce inequality by redistributing money from the rich to the poor face the dilemma that in doing so (by increasing tax rates and means-tested benefits, for example) they reduce the incentive for individuals to increase their incomes. Policy-makers have tried to balance these objectives in different ways and, partly as a result of this, the tax and benefit system today is very different from the one that existed thirty years ago. In this paper we look at how the tax and benefit system redistributed income and affected incentives to work in 2009-10, and at the effect of tax and benefit reforms between 1978-79 and 2009-10 on the level of inequality and work incentives.

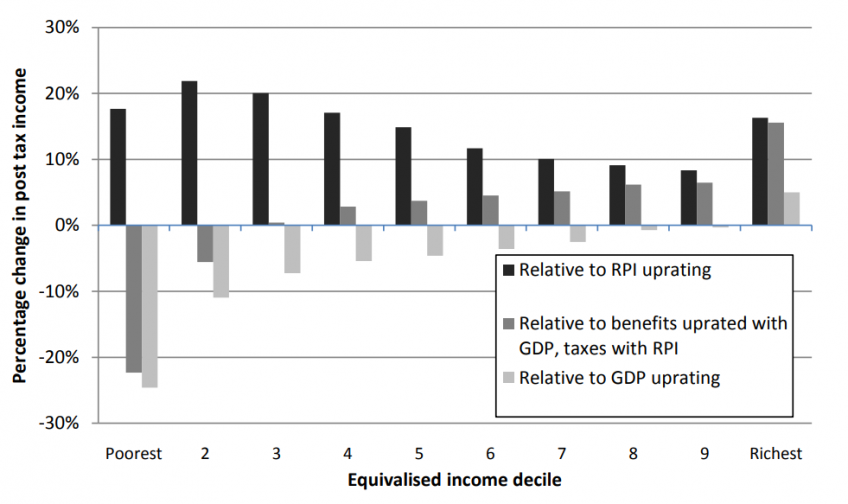

Figure: Distributional impact of tax and benefit reforms from 1978 to 2009

Notes: Households divided into ten equally sized groups based on their disposable income, adjusted for family size. Assumes full take-up of means-tested benefits. Excludes most ‘business taxes’ (notably corporation tax and business rates, though not employer National Insurance contributions) and capital taxes (notably inheritance tax, stamp duties and capital gains tax). Source: Authors’ calculations using TAXBEN run on uprated data from the 2005–06 EFS.

Authors

Stuart Adam

Stuart is a Senior Economist working in the Tax sector, and focuses on analysing the design of the tax and benefit system.

James Browne

More from IFS

Understand this issue

Policy analysis

Academic research