Summary

Today’s Government Expenditure and Revenue Scotland (GERS) figures show Scotland’s implicit budget deficit increasing to 8.6% of GDP in 2019-20, around 6 percentage points higher than the UK as a whole, largely reflecting higher government spending. The Covid-19 crisis means that figures for the current and next few years are likely to differ massively though. Indeed, the UK’s actual and Scotland’s implicit budget deficit this year could spike at almost 19% and 26-28% of GDP respectively, based on Office for Budget Responsibility projections. And ongoing economic weakness means that the deficits will likely remain elevated even in 2024-25. With this in mind, this observation looks at what we can learn from the GERS figures and what might be in store over the next few years.

Introduction

Over the last decade, the publication of Government Expenditure and Revenue Scotland (GERS) has become a key event in Scotland’s political diary. The figures have proved contentious, but while subject to a degree of potential measurement error, their status as National Statistics means they have been independently assessed as being based on sound methods and being produced free from political interference. And while backwards- rather than forwards-looking they do provide the most sensible starting point for assessing the kind of fiscal challenges and opportunities that Scotland would initially face under full fiscal autonomy or independence, as recognised by the SNP’s Sustainable Growth Commission.

So, what can we infer from this year’s GERS figures about Scotland’s fiscal position? And how might things evolve in the light of the economic and fiscal impact of the Covid-19 crisis?

Scotland’s implicit budget deficit increased in 2019-20 and was substantially higher than that of the UK as a whole

The difference between revenues raised and government spending in or on behalf of Scotland is estimated to have been 8.6% of GDP in 2019-20. This is up from 7.4% in 2018-19, and is the first increase since 2015-16, when lower oil prices led to a slump in North Sea revenues. The increase again is partly driven by a fall in North Sea revenues, which accounts for about 0.4 percentage points of it. A fall in North Sea output also meant total Scottish GDP is estimated to have fallen slightly, pushing up Scotland’s implicit budget deficit when measured as a percentage of GDP. But around half of the increase in the implicit deficit reflects what happened onshore. Government expenditure increased by 1.1% above inflation, the fastest increase since 2010-11, as the UK government started to loosen the spending taps after nine years of austerity. On the other hand, onshore revenues declined by 0.2%, driven by weak income tax, VAT and corporation tax receipts.

An increase in government spending and a stalling of revenue growth (driven by the same tax types) also led to the first increase in the budget deficit for the UK as a whole for a decade: up from 1.9% of GDP in 2018-19 to 2.6% of GDP in 2019-20. But Scotland’s deficit of 8.6% of GDP is a full 6.0 percentage points of GDP higher, a gap equivalent to almost £11 billion. Total borrowing is equivalent to £2,776 per person in Scotland, compared to £855 per person across the UK as a whole.

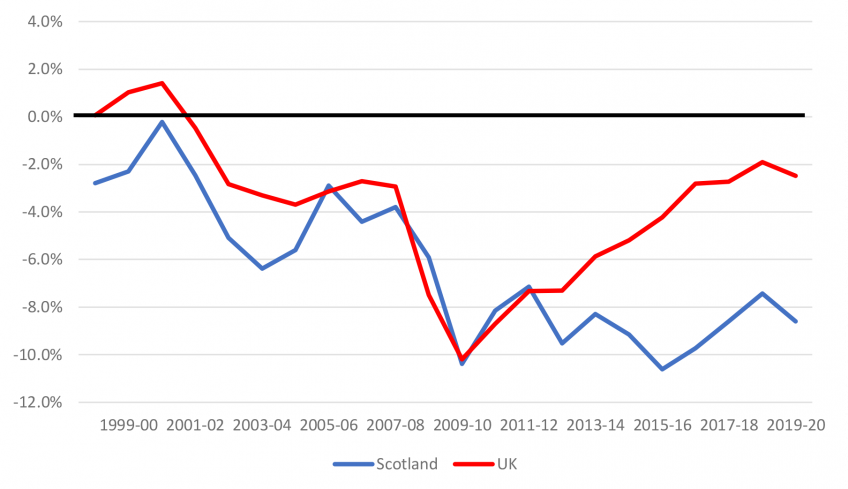

Figure 1 shows that Scotland’s implicit budget deficit has been consistently higher than that of the UK as a whole since 2012-13, with the gap amounting to between 5% and 7% of GDP every year since 2015-16.

Figure 1. Scottish and UK budget deficits, % of GDP, 1998-99 to 2019-20

Notes: Positive figures are surpluses, negative figures deficits. Deficit measure is the Net Fiscal Balance including a geographic share of North Sea revenues for Scotland.

Source: Government Expenditure Revenue Scotland 2019-20.

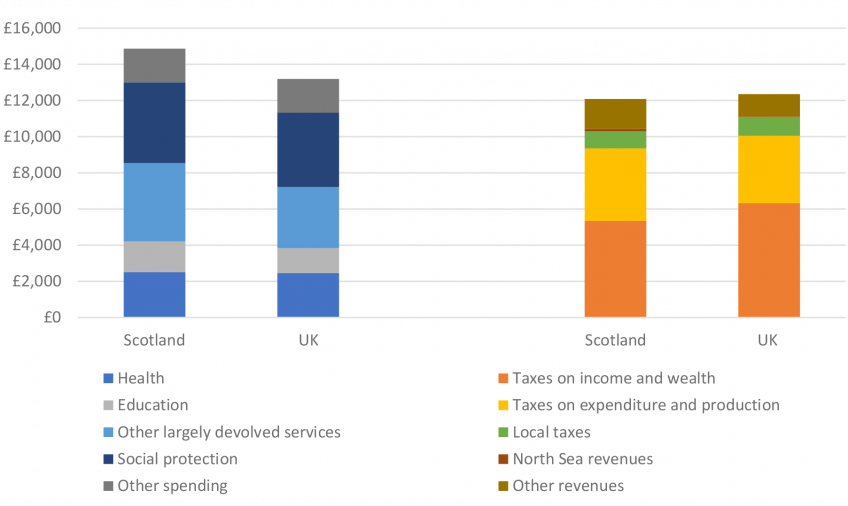

This fiscal gap reflects the fact that government spending in or on behalf of Scotland (£14,829 per person) is around 12% higher than for the UK as a whole (£13,196). Figure 2 shows that this higher spending is driven by spending on services that are largely devolved to the Scottish Government. This is particular true for education, where spending per person is around 22% higher than for the UK, and other non-health services (such as culture, housing and transport) where it is 29% higher. Conversely spending health is only around 3% higher, and spending on social protection – which includes benefits, tax credits and social care services – is around 8% higher. Previous analysis shows that spending on benefits and tax credits is in fact even closer to the national average, reflecting the fact that Scottish household incomes are close to the national average. Spending on the social care component of this is substantially higher though, partly reflecting a policy of free personal care for the elderly.

In contrast, the Figure shows that revenues, even including those from the North Sea, are around 2.5% below the UK average (£12,058 versus £12,367). This reflects lower revenues from taxes on income and wealth, which is only partly offset by higher revenues from taxes on expenditure and production and various accounting adjustments.

Figure 2. Comparison of government spending and revenues per capita, UK and Scotland, 2019-20

Note: See methodology section of this observation for definitions of spending and revenue categories.

Source: Government Expenditure Revenue Scotland 2019-20.

As we and other commentators have noted previously, most regions’ tax revenues per person lag the UK average, which is dragged up by the very high amounts raised in London and to some extent the South East of England. However, Scotland stands out as having much higher levels of government spending than the East of England and South West of England, which have similar income levels (and raise similar levels of revenues per person). This is a pattern that goes back decades and reflects the relatively generous levels of block grant funding for devolved services received by the Scottish Government.

What about 2020-21 and beyond?

Of course, much has changed over the last few months and borrowing figures for the current financial year, 2020-21, while still highly uncertain, will far exceed the figures for 2019-20 reported today. Indeed, they are almost certain to be a peace-time record.

The Office for Budget Responsibility (OBR) has not published a full set of updated forecasts since before the full scale of the Covid-19 crisis became evident. However, as part of its Fiscal Sustainability Report looking at the long-term outlook for the public finances, it published central, optimistic and pessimistic scenarios for the period to 2024-25. And it has more recently published estimates of the impact of additional tax and spending measures announced in the UK Chancellor’s Summer Economic Update. We can use these scenarios and estimates to look at how the UK and Scotland’s budget deficit may evolve over the next 5 years, bearing in mind the particular levels of uncertainty at the moment, both economic and in terms of future policy measures.

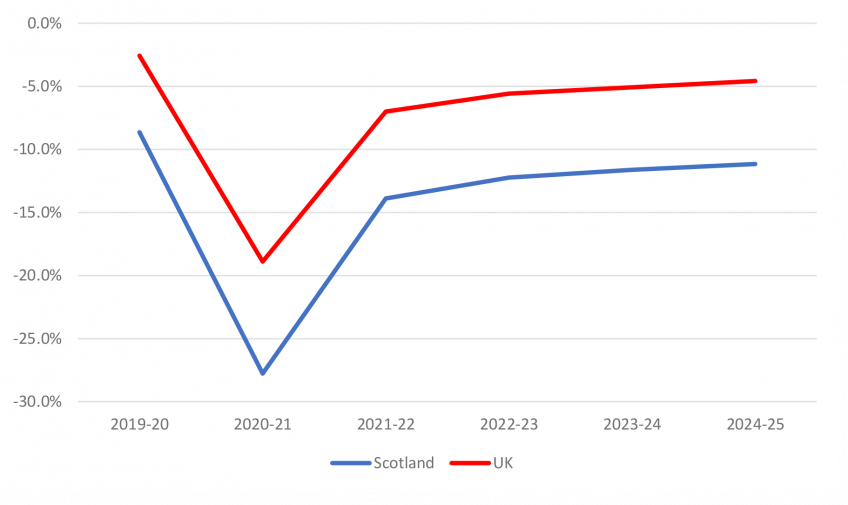

Figure 3 does this, using the OBR’s central scenario. It shows the UK’s budget deficit spiking at almost 19% of GDP in 2020-21, or £372 billion in cash terms. This would mean the UK government borrowing 33p of every £1 it spends, compared to a maximum of 22p at the height of the impact of the late 2000s financial crisis in 2009-10.

More than half of this is accounted for by the temporary tax cuts and spending increases enacted by the government to support businesses, households and public services through the Covid-19 crisis. But a substantial part reflects shortfalls in revenues and higher spending on benefits as a result of a weaker economy – and the OBR and other forecasters, expect this to persist. Hence, even by 2024-25, the UK’s budget deficit is projected to be 4.6% of GDP, over double what the OBR was forecasting prior to the Covid-19 crisis.

Figure 3. Projections of Scottish and UK budget deficits, % of GDP, 2019-20 to 2024-25

Notes: Positive figures are surpluses, negative figures deficits. Deficit measure is the Net Fiscal Balance including a geographic share of North Sea revenues for Scotland. See methodology note for information on projection methodology.

Source: Government Expenditure Revenue Scotland 2019-20, and the Office for Budget Responsibility’s Fiscal Sustainability Report and Policy Monitoring Database.

Scotland’s economy and implicit budget deficit are unlikely to follow exactly the same path as that of the UK as a whole. However estimates suggest Scotland and the UK as a whole have followed very similar economic trajectories so far, so assuming they follow the same fiscal path going forwards seems a reasonable central assumption. Assuming that Scotland’s public finances were to evolve in line with the OBR’s central scenario for the UK as a whole, Figure 3 shows that the implicit budget deficit would reach almost 28% of GDP this year if spending per person increases at the same percentage rate as the UK as a whole and just over 26% if it increases by the same in cash terms. Moreover, it would still exceed 11% of GDP in 2024-25. The latter is a very high level, probably exceeded by the UK government in only one year since the end of World War II: the current one.

Of course, these figures are far from certain. And it is worth noting that the implicit deficits of Wales and Northern Ireland will almost certainly be even higher than Scotland’s, reflecting their weaker economies and lower tax revenues (and, in the latter case, even higher government spending). And the deficit is likely to be broadly similar to Scotland in the North and Midlands of England. Scotland is therefore far from unique among the regions and nations of the UK in the scale of its gap between tax revenues and spending.

What are the implications of these figures for policy?

What is unique though is the intense debate about Scotland’s fiscal framework and constitutional future.

Both the overall UK deficit and the implicit Scottish deficit are, under current fiscal and constitutional arrangements, almost entirely the responsibility of the UK government. The Scottish Government’s borrowing powers are limited to £450 million for capital investment and either £300 million or £600 million, depending on circumstances, to address volatility and forecast errors for devolved taxes, such as income tax and land and buildings transactions tax. As highlighted previously, there is a case for granting additional borrowing powers, at least temporarily. And figures for income tax revenues in 2018-19 to be published next month are likely to show existing limits can be constraining even in more benign times, so longer-term reform may also be warranted.

If the OBR’s central scenario is correct, the UK government will almost certainly have to increase taxes or hold down spending in order to reduce its budget deficit and halt the rise in government debt. These measures would inevitably impact on Scotland, although the Scottish Government’s devolved tax powers would allow it some flexibility to vary the mix of tax rises and spending restraint if it so wished, as it has done in recent years.

Under full fiscal autonomy or independence, the deficit would be the Scottish Government’s responsibility, and the need for tax rises or spending cuts would be starker. The SNP’s Sustainable Growth Commission proposed holding down overall growth in public spending to 0.5% for a decade – implying cuts to areas other than health, social care and pensions – to reduce Scotland’s budget deficit to less than 3% of GDP. The likely long-run hit to the public finances as a result of the Covid-19 crisis would mean that spending restraint would have to be even more stringent and/or long lasting, or be accompanied by tax increases.

That does not mean Scotland cannot afford to be independent, nor that there aren’t opportunities for better policy to improve performance and better address Scottish needs and preferences. If such policies can be developed and implemented, this could ultimately allow more to be spent on public services and more to be kept in Scottish people’s pockets in the longer term. It is just that the Covid-19 crisis has made the immediate public finance situation more challenging.

Notes on methodology for projecting Scotland’s fiscal position beyond 2019–20

In order to project forward the GERS 2019–20 figures to the period covering 2020–21 to 2024–25 using figures from the OBR’s central reference scenario for the public finance scenarios as updated to account for measures announced in the Summer Economic Update, the following method is used:

• Spending is projected forward assuming that amount spent per person in Scotland grows in line with amount spent per person in the UK as a whole. This means spending per person in Scotland is projected to be 112.5% of the average for the UK as a whole, as in 2019–20. As an alternate scenario, we assume spending per person in 2020-21 increases by the same amount in cash terms as the UK as a whole.

• Onshore taxes are projected on the basis that the amount paid per person in Scotland grows in line with forecast growth in onshore revenues per person for the UK as a whole. This means onshore tax revenues per person in Scotland are projected to be 97.5% of the average for the UK as a whole, as in 2019–20.

• Offshore (oil and gas) taxes are projected under the assumption that Scotland’s share of overall UK offshore tax revenues remains the same as in 2017–18 at 111.4% (i.e. revenues from the rest of the UK are projected to be negative as they were in 2019–20).

We have chosen the assumptions on the basis of their simplicity and as a reasonable baseline case. As with any economic or fiscal forecast or projection, the projections outlined in this observation will differ from eventual outturns. This includes the OBR scenario for the UK as a whole; and trends in spending and government revenues in Scotland relative to the UK.

An alternative approach would have been to try to model the additional funding the Scottish Government is receiving via the Barnett formula and additional top-ups such as those announced on July 24th. However, the lack of a full up-to-date dataset of this additional funding makes such an approach difficult.

Notes on methodology for classifying spending and revenues in Figure 2

Revenues included in each revenue category:

• Taxes on income and wealth are: income tax, National Insurance contributions, onshore corporation tax, capital gains tax, inheritance tax, stamp duties and land and building transactions tax.

• Taxes on expenditure and production are: VAT, fuel duties, excise duties, air passenger duty, vehicle excise duties, insurance premium tax, environmental levies, Scottish landfill tax, and ‘other taxes’.

• Local taxes are: non-domestic rates and council tax.

• North Sea taxes are taxes levied on the profits and revenues of North Sea oil and gas operations.

• Other revenues are: interest and dividends, gross operating surplus and ‘other receipts’.

Expenditures included in each expenditure category:

• Health, education and social protection spending are taken directly from GERS.

• Other largely devolved spending is those spending categories where at least 50% of spending is undertaken by the Scottish and local government, excluding health and education. These categories are: public and common services, public order and safety, enterprise and economic development, agriculture, forestry and fisheries, transport, environmental protection, housing and community amenities, recreation, culture and leisure, and accounting adjustments.

• Other spending is all remaining spending.

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

More from IFS

Understand this issue

Policy analysis

Academic research