Automatic enrolment has been hugely successful, such that over 90% of eligible private sector workers are now members of workplace pension schemes. Given they started furthest behind in terms of pension provision, it is not surprising that the biggest increases in coverage were for the young, the low-paid and the financially insecure. What is more surprising, and perhaps worrying, is that there is now no difference in participation rates at all across groups with different levels of financial security. Even among the least financially secure 3% of eligible private sector employees – those with little or no savings, unable to afford necessities, on very low incomes and with poor health – participation rates are above 90%. Given their current financial difficulties, it is not obvious that most in this group should be reducing their current gross earnings, even by 3%, in order to save for a pension.

The government’s automatic enrolment policy, which obliges private sector employers to enrol most employees into a workplace pension scheme, has substantially boosted pension membership: in 2019, four out of five private sector employees were saving in a workplace pension. This compares with just two out of five in 2012, prior to automatic enrolment being introduced. Given the objective of bringing more employees into workplace pension saving, this is broadly a big policy success.

Importantly, pension saving under automatic enrolment is not compulsory – employees can still choose to opt out. Automatic enrolment encourages pension saving through at least three mechanisms: it has increased the availability of workplace pension schemes, it provides a financial incentive in the form of employer contributions and it makes membership the default for eligible employees.

Research recently published by IFS (Bourquin et al., 2020[1]) showed that the last mechanism – making pension membership the default – has had especially strong effects, particularly boosting pension participation amongst employees who had relatively low participation prior to automatic enrolment. This includes, for example, younger employees, those with lower earnings, those with lower levels of education, and renters. Most of the increase in overall pension participation under automatic enrolment is from people who are relatively financially secure and likely to have good reasons to remain in a workplace pension scheme. However, part of it is driven by a substantial increase in participation among employees who appear to be less financially secure. This is potentially worrisome, given that many of these individuals could be better off leaving their pension scheme (perhaps temporarily) in favour of higher take-home pay to, for example, boost current consumption, save for a ‘rainy day fund’ or pay off costly debts.

That research analysed data up to 2017–18. In April 2018, the minimum contribution required under automatic enrolment increased from 2% of qualifying earnings (of which at least 1% had to be from the employer) to 5% (of which at least 3% had to be from the employer). This is potentially important, as employees may be more likely to opt out when their contribution rates are higher – arguably especially so if they are financially insecure. We therefore now extend the analysis using newly released data to examine whether behaviour differed in 2018–19.[2]

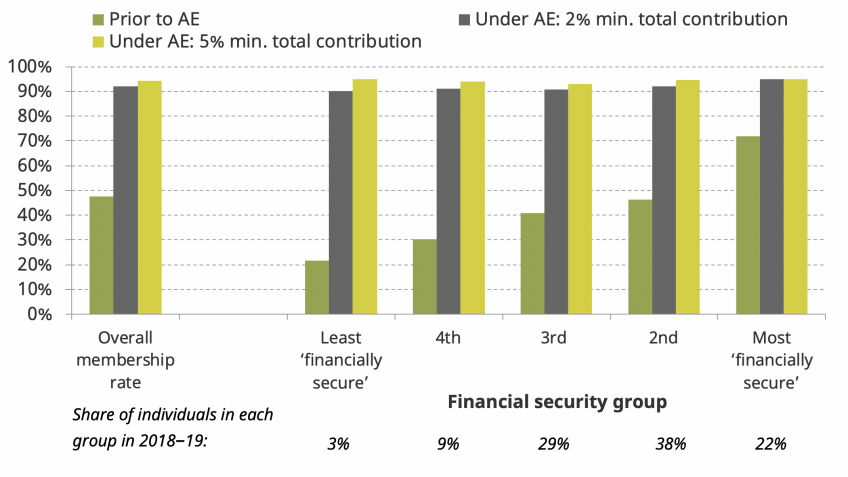

Figure 1 presents the workplace pension participation rate for eligible employees observed prior to the introduction of automatic enrolment (AE) as well as for those observed since its introduction. For the latter group, we show participation rates separately for those observed up to March 2018 (when the minimum total contribution rate was 2%) and for those observed in 2018–19 (when the minimum total contribution rate was 5%). Automatic enrolment increased pension membership across all eligible employees from under 50% to over 90%, and there is no evidence that membership rates fell in 2018–19 despite the increase in contribution rates.

Figure 1: Workplace pension participation of eligible employees

Note: Eligible private sector employees only. The financial security groups are defined in the endnote and in Bourquin et al. (2020). Due to data constraints, ‘Prior to AE’ refers to the period April 2011 to September 2012, ‘Under AE: 2% min. total contribution’ refers to the period February 2014 to March 2018, and ‘Under AE: 5% min. total contribution’ refers to the period April 2018 to March 2019.

Source: First two bars in each set as in figure 9 of Bourquin et al. (2020), using the Family Resources Survey, 2011–12 to 2017–18. Third bars are authors' calculations using the Family Resources Survey, 2018–19.

The figure also shows pension membership over time for five groups of employees with varying degrees of financial security (as measured by several financial, material deprivation and health indicators).[3] Prior to automatic enrolment, pension participation was considerably lower amongst those who appear less financially secure. Only 22% of the least financially secure (by our measure) were in a pension as compared with 72% of the most financially secure. Under automatic enrolment, however, the pension participation rate of the least financially secure is above 90% and very similar to that of the most financially secure (95%). This remains true in 2018–19, after the minimum default contribution rate has increased. It should be noted that very few – just 3% – employees are in this ‘least financially secure’ group; but it still represents a large number of employees across the UK.

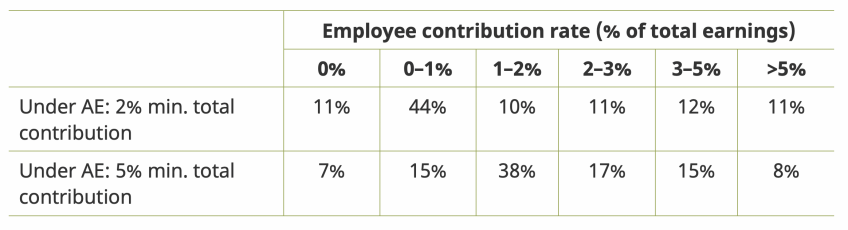

As shown in Table 1, the high workplace pension participation rate of the least financially secure employees is not explained by them having negligible (or even no) employee contributions (which could occur under automatic enrolment if their employer is contributing the entirety of the minimum total contribution). In 2018–19, 40% of the eligible employees we define as being part of the ‘least financially secure’ group, and who were members of a workplace pension, reported employee contribution rates of more than 2% of total earnings, with 8% reporting contributing more than 5% of earnings. This suggests that many are being defaulted in at (or are actively choosing to contribute) a higher level of contribution than the legal minimum required under automatic enrolment.

Table 1: Distribution of employee pension contribution rates of the least financially secure

Note: Eligible private sector employees who remain in a workplace pension that they were automatically enrolled into. The financial security groups are defined in the endnote and in Bourquin et al. (2020).

Source: Authors’ calculations using the FRS, 2012–13 to 2018–19.

The increase in minimum total contribution rates in 2018–19 does not appear to have led to a rise in opt-outs among the least financially secure. Given this, it seems reasonable to suppose that there was also no increase in opt-outs after the final increase in minimum contribution rates that happened in April 2019 (when the minimum total contribution rate increased to 8% of qualifying earnings, with at least 3% to come from the employer). The concern therefore remains that the strong nudge of automatic enrolment – that has rightly been hailed as successful in bringing many more into pension saving – has a downside. It changes the behaviour of a small number of individuals in a way that might well not be in their best interests.

It is not clear why the small number of people who would probably be better off not sticking with the default, and instead opting out of pension saving (at least temporarily), do not do so. The defaulting aspect of automatic enrolment has been shown to be powerful, but it is unclear whether that is because individuals do not know they can opt out, or they do not know how to, or they cannot be bothered for the amounts of extra take-home pay they would receive. The average gross earnings among the least financially secure group in 2018–19 were £357 per week, so ceasing pension contributions at 5% of their gross qualifying earnings (equivalent on average to over 3% of total earnings) would on average raise take-home pay by around £12 per week. It is also a difficult issue for policymakers to address, since taking advantage of inertia in individuals’ decision-making is what has made automatic enrolment so successful, to the advantage of large numbers of employees.

This is an issue that could become more salient over the coming months. Many are experiencing falls in earnings due to the public health response to the COVID-19 pandemic, while plummeting share prices and interest rates will also have led to lower incomes from savings and investments. The proportion of automatically enrolled employees who are financially vulnerable could therefore increase. One option for employees currently struggling financially is to temporarily leave their workplace pension scheme in favour of higher disposable income. But whether this is an option that individuals are aware of and choose to exercise remains to be seen.

Endnote

Construction of ‘financial security index’

We first define four potential indicators of severe financial difficulty: (1) being in the lowest tenth of the distribution of working households’ equivalised income (after deducting housing costs); (2) being in the most materially deprived tenth of eligible employees; (3) having (in combination with one’s partner, where relevant) less than £1,500 in liquid savings; and (4) having a long-standing health issue that limits daily activities.

We also define a set of conditions that, if all are fulfilled, suggests an individual is financially secure. These include having liquid financial assets of at least £8,000 (combined with a partner, where relevant), not currently being behind on any bills, belonging to the top half of the distribution of working households’ equivalised income (after deducting housing costs) and belonging to the top half of the individual gross earnings distribution of employees.

We then combine the four financial difficulty indicators and the one financial security condition to create a ‘financial security index’ with five groups, ordered from most to least financially secure:

- most ‘financially secure’: meet the ‘financial security’ condition and have none of the ‘financial difficulties’ (22% of the 2018–19 AE sample);

- 2nd: do not meet ‘financial security’ condition, but have none of the ‘financial difficulties’ (38% of the 2018–19 AE sample);

- 3rd: have one ‘financial difficulty’ (29% of the 2018–19 AE sample);

- 4th: have two ‘financial difficulties’ (9% of the 2018–19 AE sample);

- least ‘financially secure’: have at least three ‘financial difficulties’ (3% of the 2018–19 AE sample).

Acknowledgements

The authors are grateful for funding from the IFS Retirement Saving Consortium, which is comprised of Age UK, Association of British Insurers, Aviva UK, Canada Life, Chartered Insurance Institute, Department for Work and Pensions, Investment Association, Legal and General Investment Management, and Money and Pensions Service. The authors are also grateful for co-funding from the ESRC-funded Centre for the Microeconomic Analysis of Public Policy (ES/M010147/1). This work is based on analysis of the Family Resources Survey data, which were made available by the Department for Work and Pensions. Thank you to Carl Emmerson, Paul Johnson, and members of the IFS Retirement Saving Consortium, for helpful comments. All views, and any errors, are those of the authors.

[1] P. Bourquin, C. Emmerson and J. Cribb, ‘Who leaves their pension after being automatically enrolled?’, 2020, IFS Briefing Note BN272, https://www.ifs.org.uk/publications/14742.

[2] The analysis in this observation uses data from the Family Resources Survey (FRS), a survey of around 20,000 households per year which is made available by the Department for Work and Pensions (DWP). For a more detailed data description, see section 3 of Bourquin et al. (2020).

[3] See section 5 of Bourquin et al. (2020) for a full description of the construction of the five financial security groups.

Authors

Rowena Crawford

Pascale Bourquin

More from IFS

Understand this issue

Policy analysis

Academic research