We are living through an unprecedented economic crisis. The government has responded with an unprecedented package of support. Fiscal measures have run up a price tag of over £100bn in just a few months. Over half of this will be spent directly supporting incomes. Around £30bn is being spent on cancelling business rates bills and providing cash grants for some firms. More will be spent if tax deferrals result in less tax being paid or loans are defaulted on. And all of the spending on the specific measures announced in response to Covid-19 will come on top of the rise in benefit payments and fall in tax revenues that naturally result from an economic contraction. Given that we have effectively shut down large parts of the economy, we expect the fall in revenues to be huge, and to have persistent effects as, for example, the carry-forward of losses depresses future revenues.

More critical decisions lie ahead

In the coming months, the government will have to decide whether to extend any of the current measures, either for a longer period or to cover more people or businesses. As the health crisis eases and lockdown is relaxed, there will undoubtedly be calls to use the tax system to help revive certain industries or parts of the economy. There may or may not be a case for some targeted fiscal stimulus – and a role for tax within that – beyond the effects of removing current constraints on activity. It is too early to say. But it is almost certain that most of the calls to help a specific industry will amount to special pleading and should be rejected.

There is uncertainty about the ultimate economic price tag of the Covid-19 crisis, but it is already huge, and it could get much bigger. It is certain we will be left with a much larger government debt and a debate about the extent to which taxes need to be raised. We entered the crisis with tax revenue already at its highest share of national income (34%) since the early 1980s. But we have also just had a decade of austerity in public spending and have an ageing population that is demanding more, and more expensive, healthcare. This crisis will lead to further demands for spending on health, social care and the social safety net. The government always has a choice over the size of the state, but the crisis undoubtedly increases the pressure for higher taxes in the long run.

Decisions about the extent of support measures in the short run, and in the longer run how much tax to raise and from whom, are critically important. Ultimately, they will determine how the financial pain created by Covid-19 is shared between different people and across different generations.

Decisions about the structure of taxation are equally important. Changes in patterns of work, transport and consumption that last beyond the immediate crisis might throw up new issues for tax policy. There are also areas of tax that were already in need of reform and have been highlighted by the crisis. Two stand out: how to tax people who work for their own businesses and how to reform business rates.

Should higher taxes on the self-employed be the price for support during the crisis?

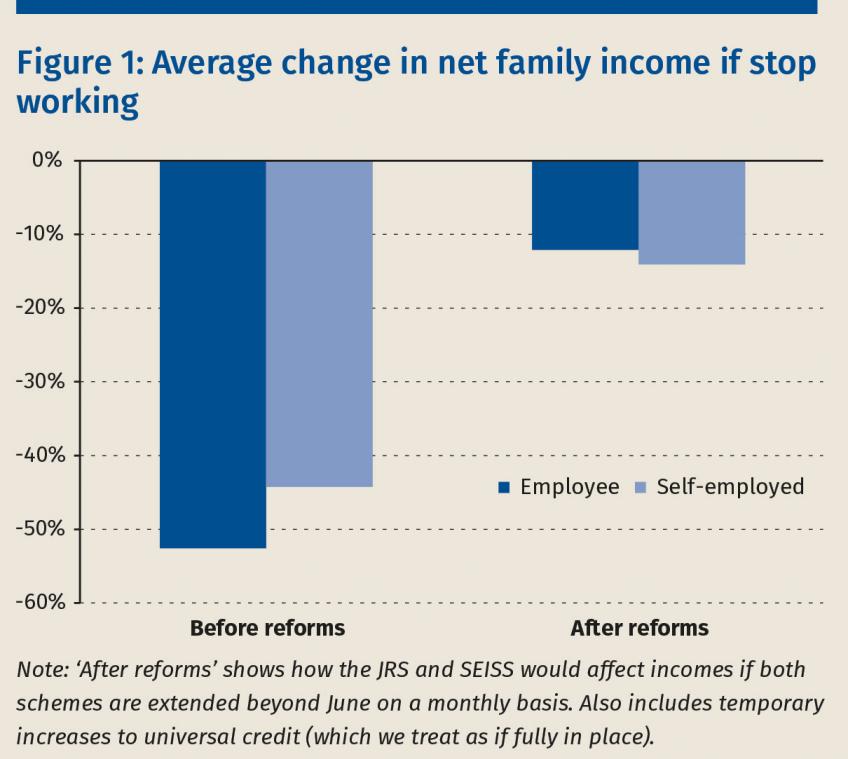

Most of the self-employed are eligible for a grant of 80% of their ‘normal profits’ (technically, 80% of three months’ worth of their average profits from April 2016 to April 2019). There are important differences between this self-employment income support scheme (SEISS) and the coronavirus job retention scheme (CJRS) for furloughed employees. For example, the CJRS is available only to employees who stop working in that job, whereas grants to the self-employed will be paid even where people continue to work and report only a small drop in profits as a result of Covid-19. There are people who fall through the gaps in both schemes. But the government is trying to provide broadly comparable insurance by replacing 80% of earnings for both employees and the self-employed. Figure 1 below shows that before the recent reforms, both employees and the self-employed would have lost about half of their net family income, on average, if they had to stop working; the JRS and SEISS reduce that to around 10% for both groups.

There is a clear pitch that the government could make following the crisis and that the chancellor laid the groundwork for when announcing the SEISS. He said: ‘in devising this scheme – in response to many calls for support – it is now much harder to justify the inconsistent contributions between people of different employment statuses. If we all want to benefit equally from state support, we must all pay in equally in future.’ Read: taxes on the self-employed will be increased to be (at least more) in line with taxes on employees.

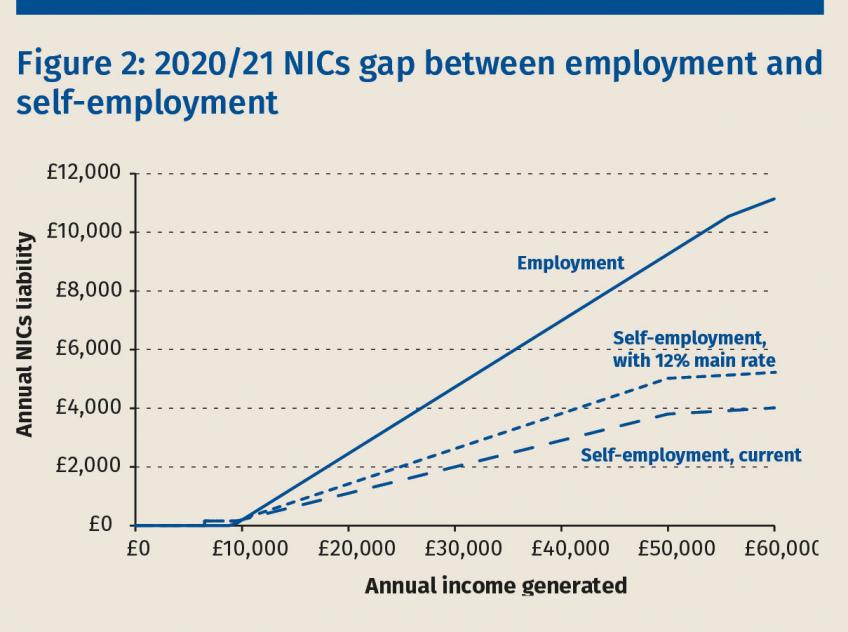

There are large tax differences between employees and the self-employed driven by NICs. The main rate of self-employed (class 4) NICs is 9%. In contrast, work that happens through an employment contract attracts both employee NICs (main rate 12%) and employer NICs (13.8%). Self-employed NICs was expected (before the crisis) to raise £3.4bn in 2019/20; that is £5.6bn less than if self-employment income was taxed at the same rates as employment income.

Perhaps the easiest sell post-crisis would be to raise class 4 NICs to 12%. This would still leave a big tax advantage for the self-employed (see figure 2 below) as they would still face no equivalent of employer NICs. Attempting even this looks optimistic based on recent history: in 2017, the government tried and failed to raise class 4 NICs to 11%. Arguably it missed a trick by not linking this attempted move towards equalisation of tax rates to the equalisation of pension rights that happened in 2016, which was a significant increase in generosity to the self-employed. Now that employees and the self-employed accrue the same rights to a single-tier state pension, only tiny differences in the two groups’ access to publicly funded benefits remain. The SEISS provides another opportunity to peg equal support from the state to equal tax payments: the crisis has shown that, not only are standard state benefits almost as generous to the self-employed as to employees, but the unspoken promise of emergency support the government provides to the self-employed is comparable to that for employees.

The government could be more ambitious and take a bigger step towards the larger reforms that are needed. The tax penalty on employment is unfair, adds complexity and means that tax shapes the structure of work. In a well-designed system, the overall marginal tax rate schedules for different forms of income should be aligned (and the tax base should be designed so that taxes do not disincentivise investment). Contrary to common belief, lower tax rates on business owners (the self-employed and company owner-managers) cannot be justified by differences in employment rights (see ‘Tax in a changing world of work’ (Helen Miller), Tax Journal, 20 April 2017). Employment rights are a cost to employers as well as a benefit to employees, so do not skew the labour market overall in favour of employment. An extra pound of income should be taxed in the same way regardless of the legal form in which it’s earned.

Alignment of tax across different legal forms implies, among other things, that self-employed NICs should be aligned with the combined rate of employee and employer NICs, which comes to 22.7%. Many baulk at this idea. But employer NICs affect the cost of hiring an employee relative to using the services of the self-employed or a company instead. This discourages employment and allows the self-employed and company owner-managers to charge more for their services than an employee could. It is the overall tax levied on different forms of income that needs to be equalised. If the government chooses to increase class 4 NICs rates after the crisis, it could, therefore, justify going much further than 12%. (Reducing employer and employee NICs could also play a part in achieving closer alignment: it need not involve simply increasing taxes.) Why settle for a small change if the political mood allows more progress to be made?

There is an equally compelling case in favour of increasing taxes on company owner-managers (for example by increasing dividend taxes, and again with a view to aligning overall marginal rates on all forms of income). Higher taxes on the self-employed would make this case stronger by increasing the tax incentive to incorporate.

Increasing taxes on company owner-managers in the aftermath of the crisis might be a harder sell politically than for the self-employed given that – at least at the time of writing – their incomes are not as well covered by the support schemes. Most company-owner managers follow a tax-advantaged strategy of paying themselves a small salary and taking most of their income in dividends. They are eligible for the CJRS for their salary from the company if they furlough themselves. This payment would be more valuable than statutory sick pay or the basic element of universal credit, but less valuable than if all of their income were covered. Despite this, crisis or no crisis, aligning taxes across different legal forms is the right thing to do.

In our opinion, the best outcome post-crisis would be for the government to set out a strategy for how to tax different forms of income and lay out a roadmap for getting there over a number of years. This would aid transparency, help taxpayers to plan, facilitate discussion of a range of related tax issues and reduce the risk of ad hoc moves in the wrong direction. What the government should absolutely avoid is giving the impression that a relatively small tax change in response to the crisis, such as adding a few percentage points to self-employed NICs, is the final ideal solution. That seems like a perfect way to shut down further reform.

Should more generous business rates relief outlive the crisis?

In this year’s Budget the government announced a fundamental review of business rates. One of the objectives is ‘reducing the overall burden’ of the business rates system, recognising concerns about its impact on the high street. The concern that business rates are killing the high street is vastly overblown. While business rates may appear to give online retailers a competitive advantage relative to those operating high street shops (and therefore paying more business rates), looking at the business rates bill in isolation gives a misleading picture. In the long run, business rates lead to lower rents (such that they are effectively paid mostly by property owners rather than occupiers). If we removed all business rates then, after a period of adjustment, rents would be higher and the total cost of premises little changed. Online competition may be a significant threat, but the existence of business rates is not driving high street decline.

In contrast, Covid-19 has actually killed the high street, at least for now while social distancing measures are in place. The government has responded by providing 100% business rates relief for businesses in England in retail, leisure and hospitality, plus an additional £25,000 cash grant if the premises they occupy have a (2017) annual rental value between £15,000 and £51,000, or £10,000 for those businesses (the majority) in any industry if their premises are worth less than that. (Similar measures have been introduced in Scotland, Wales and Northern Ireland.) Taken together, some businesses will receive over £50,000 in grant and business rates relief. These measures cost £28bn, almost as much as a full year’s business rates revenue in normal times. As temporary measures go, these are fairly well targeted at the businesses that are in most need of support.

Now that the current generous relief has been introduced, there will undoubtedly be a clamour to keep it at least in part for the longer term – adding to the pre-existing pressure to reduce business rates. Such siren calls should be resisted. If social distancing measures extend, in some form, into the next tax year, there may be a case for phasing out support gradually and avoiding large jumps in tax bills when the relief expires next April. But keeping relief in place for the long term would be expensive, and decreasingly effective as rents would rise (or perhaps not fall as they otherwise might).

After the crisis, we need to move away from temporary reliefs and look to reform business rates properly: not simply the level of the tax, but, for example, how that level should change as rents do, and how to reduce the disincentives the existing system creates to develop and invest in business property. The review announced in the Budget is explicitly intended to address such fundamental issues as well as reducing the overall burden of the tax. It is currently due to report by the autumn, and whether that timetable is stuck to or extended in light of current circumstances, the review looks opportune. Again, the Covid-19 crisis and the radical measures taken in response could provide the impetus to think radically about reform.

It would be a shame to let a serious crisis go to waste

There aren’t many upsides to the current situation. Using it as an opportunity to fix some bits of our tax system could be a silver lining, not just for people who spend their lives thinking about tax but for the nation: a well-designed tax system creates fewer distortions and allows us to raise more money with less pain. Reforms could also put us in a better position to weather the next crisis (they do, after all, tend to come around about once a decade). Permanent policy changes shouldn’t be made in response to the crisis alone. They should also address the many, broader problems that existed before the crisis. Settling for relatively easy options such as a minor tweak to self-employed NICs rates and extended business rates relief for small retailers would be a missed opportunity. To the extent that the crisis opens up scope for proper tax reform, it is a chance the government should grasp.

This article orginally appeared in Tax Journal and is used here with kind permission.

Authors

Stuart Adam

Stuart is a Senior Economist working in the Tax sector, and focuses on analysing the design of the tax and benefit system.

Helen Miller

Helen is Deputy Director of the IFS and Head of the Tax sector.

More from IFS

Understand this issue

Policy analysis

Academic research