Today the Office for National Statitics (ONS) published their March 2019 public sector finance numbers for the UK. This bulletin presents the first provisional estimates of UK public sector finances for the latest full financial year (April 2018 to March 2019).

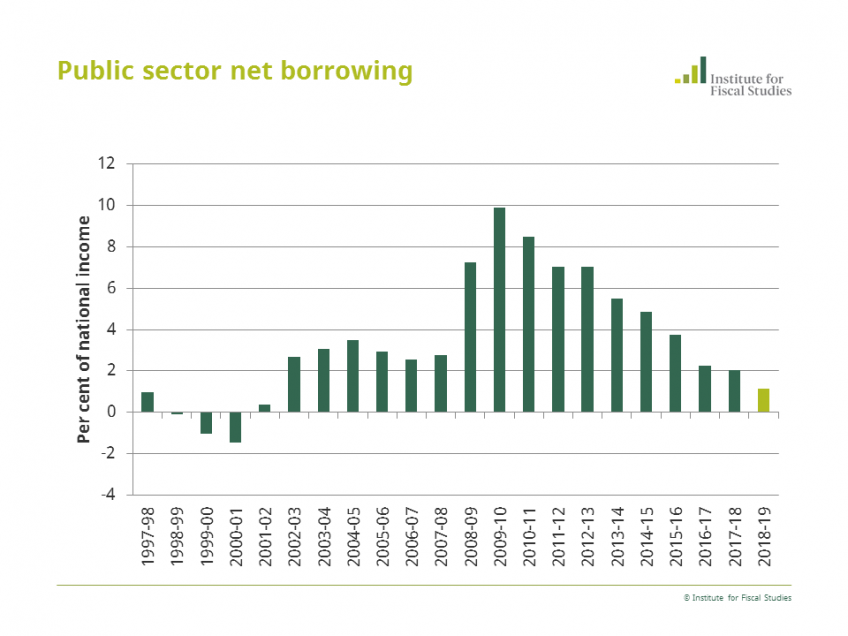

In 2018–19, the government borrowed £25 billion, or 1.2% of national income. After many years of fiscal consolidation since the financial crisis, this was the lowest deficit since 2001–02.

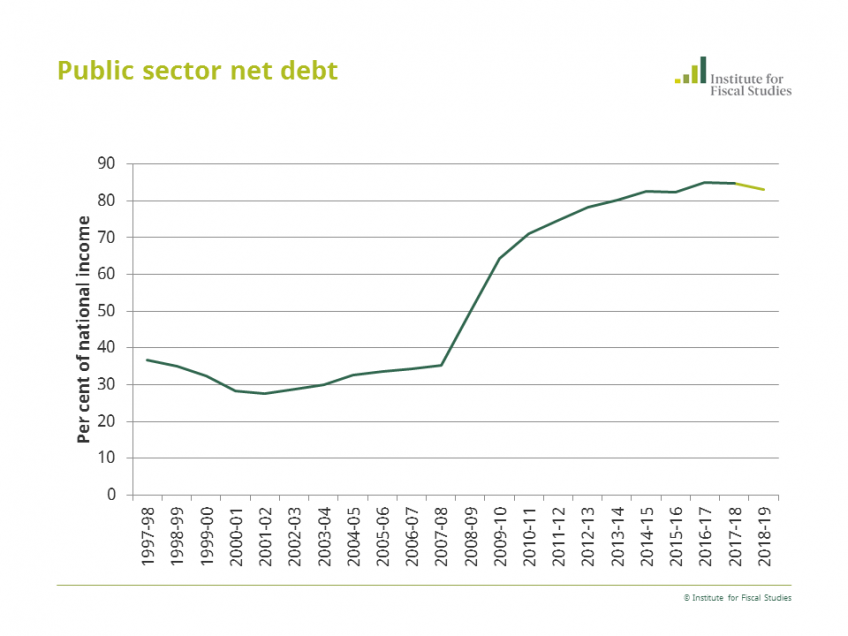

While the deficit is now below pre-crisis levels, debt remains almost 50% of national income above its 2007–08 level as a result of big deficits run since the financial crisis. Debt will remain significantly above 2007–08 levels for the foreseeable future.

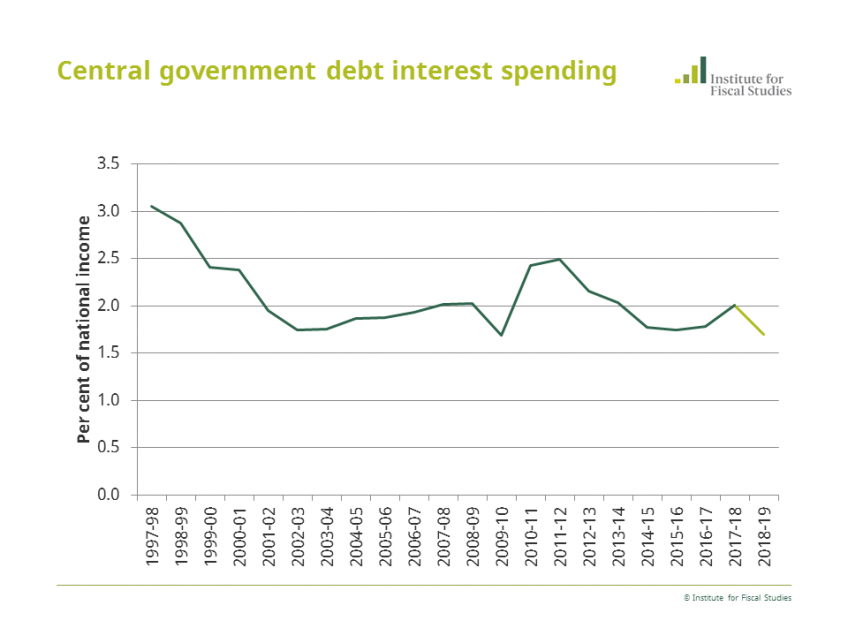

Despite debt being more than twice its 2007–08 level as a share of national income, low interest rates mean that debt interest spending is lower than it was before the financial crisis. However the public finances are now more exposed to changes in short-term interest rates than previously.

Commenting on the numbers, Research Economist Thomas Pope said:

“Today’s figures show the government borrowed £25 billion in 2018–19, slightly more than the £23 billion forecast by the OBR in last month’s Spring Statement. This is lower than the deficits run in the years leading up to the financial crisis and is the lowest deficit since 2001–02. The historically high deficits since 2008 mean that government debt is almost 50 per cent of national income higher than it was before the financial crisis, and will remain significantly above those levels for the foreseeable future. However, despite this increase debt interest costs have remained historically low due to low interest rates and the flattering accounting effect of quantitative easing. This means that the public finances are more exposed to changes in short-term interest rates than prior to the crisis.”

Authors

Thomas Pope

More from IFS

Understand this issue

Policy analysis

Academic research