Today, the Office for National Statistics has announced that it will be revising the treatment of student loans in the public finances. This is a sensible move as it aligns the accounting treatment more closely with economic reality. Even though it makes no difference to the long-run cost of Higher Education financing, the announcement has significant implications for the headline measure of the deficit, which the OBR estimates will be £12 billion higher this year, and £17 billion higher in 2023–24 as a result. In general, policy decisions should not be affected by changes in accounting treatment, but to the extent to which they are, the implications for Higher Education policy could be significant.

This observation lays out the implications of this accounting change for the public finances and government policy.

The big recent increases in tuition fees from just over £3,000 a year in 2011 to £9,250 a year today, as well as the 2016 removal of maintenance grants for students from poorer families, mean that the vast majority of undergraduate teaching is now funded through student loans. These loans are income-contingent, which means that students only start to repay the loan when their income is sufficiently high – above £25,000 in 2018–19. Even then, they only pay back 9% of their income above that level, and any outstanding debt is written off entirely thirty years after entering repayment (which is typically the first full tax year after graduation). Consequently, only around half of the total value of loans issued is expected to be repaid.

The existing accounting treatment of student loans generates a ‘fiscal illusion’ that flatters the near-term deficit considerably. Despite the large expected write-off, under the existing accounting treatment, student loans do not add to the deficit at all when they are taken out by students. This clearly has attractions for a government wanting to minimise the headline deficit, while continuing to provide up-front support to students.

Furthermore, the interest that accrues on these loans is scored as a receipt (reducing the deficit), despite the fact that the majority of that interest will never be repaid. (This may be one reason why interest is charged at up to a hefty RPI plus 3%.) This means that the net effect of the student loan system is to reduce the near-term deficit (by around £8 billion in 2023–24), even though overall policy is providing a considerable subsidy to HE students. Eventually, the unpaid loans will add to the deficit, at the point when they are written off. For the larger post-2012 loans, this will start to happen in the mid-2040s, unless the student loan book is sold off before that time, in which case the deficit would, ridiculously, never be affected by the write-off.

By contrast the government’s debt is affected in full by these loans. Student loans already account for almost £120 billion of debt and £16 billion is added each year, according to OBR figures.[1]

As far as the deficit is concerned, the change announced today aligns the treatment of student loans more closely with economic reality. When the loan is made, the new treatment will explicitly acknowledge that a portion of the transfer to students is effectively a grant – money that the government does not expect to be repaid – while the remainder is a loan which the government does expect to get back. This method is not without its complications, not least because it requires an estimate of the share of the loans that we expect to be written off rather than repaid. It will therefore be very sensitive to what is assumed about how graduate earnings will evolve in the future, which may be particularly complicated if the population of students changes significantly (for example, if the government were to restrict HE student numbers in a targeted way).

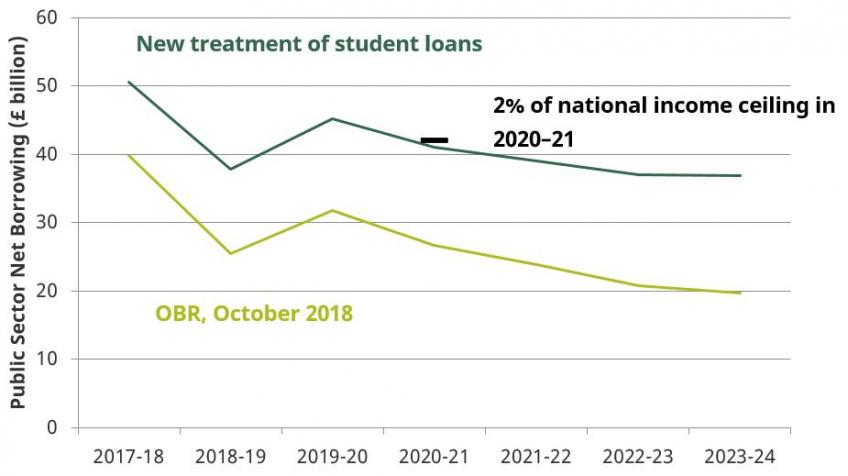

Notwithstanding these complications, however, it represents a marked improvement in how the loans are treated. Based on OBR estimates, this is likely to increase the headline measure of the deficit by around £12 billion in 2018–19, rising to £17 billion in 2023–24.

Figure: Indicative revised path for borrowing under new student loans accounting treatment

Note: 2% of national income target in 2020–21 refers to cyclically-adjusted borrowing. The ceiling has been adjusted accordingly.

Source: Chart 4.A of Office for Budget Responsibility Economic and Fiscal Outlook, October 2018 (https://obr.uk/efo/economic-fiscal-outlook-october-2018/)

Nothing to see here?

It is important to note that nothing ‘real’ changes as a result of this accounting change – the student loan system could continue to operate as it currently does, and fundamentally the public finances would be in just as strong a position as they would have otherwise been. The only change is over how and when the net subsidy from the government to students through the student loan system is scored for the purposes of the headline deficit. In principle, the government should not change its policy in response to a cosmetic change in fiscal presentation.

A similar issue arises with the government’s fiscal targets. The government was previously targeting a structural (i.e. adjusted for the estimated impact of the ups-and-downs of the economic cycle) deficit of less than 2% of national income in 2020–21, and had pledged to ‘eliminate the deficit entirely by the mid-2020s’. If those were the appropriate fiscal targets before, the government could simply adjust them for this accounting change – they could now target a structural deficit of no more than 2.6% of national income in 2020–21, and to have a deficit of below around £20 billion by the mid-2020s.

Possible effects on policy

In reality, however, this accounting change is likely to have concrete implications for government policy. The previous system appeared absurdly generous to the government in the near-term when it arranged transfers as income-contingent loans rather than as grants. Today’s accounting change makes this relatively less attractive, and as a result makes a system that is more reliant on grants appear relatively less expensive.

The government is currently conducting a comprehensive review of post-18 education. The ONS decision could affect the recommendations of that review or the likelihood that those recommendations are accepted: suddenly, the high cost of HE appears in the deficit today, rather than in 30 years time. Not only is it suddenly superficially more attractive to replace some loans with grants, it is also superficially more attractive to reduce fees or abolish them altogether (as Labour proposed in its 2017 general election manifesto), to reduce the interest rate charged on outstanding student loans, or to restrict student numbers. Those options might now be considerably more likely to be implemented: indeed, the review into post-18 education has been awaiting confirmation of the accounting treatment of student loans before reporting.[2]

One effect of this change is that the increase in the repayment threshold from £21,000 to £25,000, that was announced last year, now looks quite expensive in the short term. On the old measure it had little effect on this year’s deficit, on the new measure it increases it by around £2 billion per year. Again, the actual effect on the public finances is the same – it was just that the current accounting rules hid the short-term effect.

If the government does not choose to adjust its fiscal targets in the medium-term in response to this accounting change (as has been the case when other changes to accounting rules have affected the deficit in the past), then the implications could go further than HE policy. Maintaining the overarching fiscal objective of ‘eliminating the deficit entirely’ by the mid-2020s would – if the commitment is to be met – imply a combination of further tax rises or deeper spending cuts. Or, as is more likely, it would make it more likely that this target will be breached rather than met. Similarly, it would mean that Chancellor’s headroom against his 2% of GDP deficit target for 2020–21 would be almost eliminated (reduced from £15 billion to £1 billion), making it more likely that this target will end up being breached rather than met.

While nothing ‘real’ has changed as a result of today’s announcement, it could have substantial effects on government policy. We will learn more about what those effects might be when the government reports on its post-18 education review and reviews its fiscal plans at the Spring Statement.

[1] Source: Supplementary Table 2.1 of Office for Budget Responsibility Fiscal Sustainability Report, July 2018 (https://obr.uk/fsr/fiscal-sustainability-report-july-2018/).

[2] Source: Tuition fees review to wait on loans decision, BBC News, September 2018 (https://www.bbc.co.uk/news/education-45474557).

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Jack Britton

Jack's main interests lie in human capital accumulation and discrete choice dynamic modelling.

Thomas Pope

More from IFS

Understand this issue

Policy analysis

Academic research