This article was first published by Taxation and is reproduced here with full permission. Download a pdf version here.

The recent rise of self-employment – which accounted for 40% of the UK’s workforce growth between 2008 and 2017 – and in particular the growth of so-called ‘gig economy’ jobs has sparked fresh debate about who should have employment rights and when. A central concern is that employers are restructuring jobs in ways that leave individuals with fewer rights.

Earlier this year, Pimlico Plumbers was at the centre of this debate in the Supreme Court when Gary Smith won his case to be classed as a worker (and receive more rights) rather than as self-employed. But, to the confusion of many, Mr Smith is still self-employed for tax purposes.

Although there may be a good commercial case for contracting with self-employed plumbers rather than employing them directly, there is also a significant tax advantage. Namely, structuring jobs so that work is done though self-employment attracts a much smaller tax bill.

The Pimlico Plumbers case highlights not only that there is a blurred boundary between employment and self-employment, but that the boundaries are different in employment law – in which individuals can be employees, workers or self-employed – and tax – for which there is no equivalent to the ‘worker’ category. This situation has led to calls to align definitions across tax and employment rights so that self-employment means self-employment.

One common definition would be simpler, and simplicity has much to recommend it. But a common – and understandable – misconception is that self-employed people should pay lower taxes precisely because they do not have employment rights and, conversely, those who do have employment rights should be taxed at higher rates.

It sounds a compelling argument – employees receive benefits that the self-employed do not, why shouldn’t they pay higher taxes?

Tax cannot offset rights

It may be compelling, but it is wrong. And not wrong based on some specific notion of how the labour market works. The logic fails regardless of what one assumes about how wages adjust.

The reason is that employment rights affect both sides of the labour market – employees and employers. Employment rights can make some employees better off and make some people want to switch from self-employment to employment but they also make employers less inclined to choose employees over the self-employed. Because of this, employment rights do not – and cannot – act to skew the labour market in favour of employment.

In contrast, our tax system does skew the market in favour of getting work done through self-employment. Add together these two effects and you have a situation that skews the market in favour of self-employment, not one with a level playing field.

Labour market permutations

There are many permutations of how specific employment rights may affect employers and employees, all of which centre on two key factors. The first is how much employees value the benefits they receive as a result of employment rights – how much of their pay they would be willing to give up to acquire them – relative to how much they cost the employers to provide. The second is how wages adjust.

The easiest case to consider is when the value of rights to employees is exactly equal to the cost to employers. For example, imagine the government increases statutory paid holiday by one day. The value to the employee of an extra day off is one day’s wages; the cost to the employer is one day’s wages. How wages adjust determines whether employees or employers benefit from this new right.

If annual wages fall (or do not increase as much as they would have done) to compensate exactly for the increase in holiday and reduction in work, employees and employers may be left indifferent to the change – workers are paid the same wage for the work they do and employers are paying the same for the work they receive. If wages do not adjust at all – perhaps an employee is earning the minimum wage – employees who receive the same pay for less work are better off but employers are worse off because the cost of obtaining a specific amount of work completed has risen. This might be the desired effect – the change has given employees more power in their relationship with the employer. But, regardless of how wages adjust, employment rights have not skewed the overall labour market in favour of employment relative to self-employment: if new rights make more people prefer employment to self-employment, they will also make employers prefer the self-employed.

Mutually beneficial trades

Some rights or benefits are highly valued by employees and are relatively cheap for employers to provide. For example, employers may be able to use their economies of scale to provide healthcare to employees at a better rate than they could negotiate individually. This is a common benefit. Similarly, employers often offer more than the minimum statutory levels of holiday pay and parental benefits as part of employees’ compensation packages.

When the value of a benefit to an employee is higher than the cost to the employer, there is room for a mutually beneficial trade. The employer can provide these types of benefits in place of some cash wages and, by doing so, can make employment more attractive to both itself and staff. But, we expect employers to provide these types of benefits regardless of whether they are mandated in employment law: government intervention does not create mutually beneficial trades.

It can be the case that some rights cost more for the employer to provide than they are worth to the employee. Returning to the holiday example, imagine that, given the choice, the worker would not swap a day’s pay for an extra day’s holiday – they value the money more than the day off – but it still costs the employer a day’s wages to increase that entitlement. If wages adjusted down fully in response to an extra day of holiday, the employer would be neither better nor worse off but the employee would be worse off. If wages do not adjust at all, the employer is worse off by more than the employee is better off. In such cases employment rights can create a bias in favour of having work done though self-employment rather than employment. That is, the bias does not even go in the right direction to support the argument in favour of higher taxes on employees.

Running out of reasons

The punch line is this: even though employment rights can help specific individuals as intended, they do not result in a labour market with fewer self-employed people and more employees. Therefore it makes no sense to argue that we need to offset the non-existent bias created by employment rights by tilting the tax system in favour of the self-employed legal form. Far from creating a level playing field, lower taxes on selfemployment create an uneven one that gives employers a strong incentive to restructure work. Without the tax breaks, plenty of people would make sensible, commercial decisions to be self-employed. But more employers would be willing to offer employment positions and the associated protections they bring.

Even accepting that differences in employment rights cannot be used as a credible argument in favour of lower taxes on the self-employed, one could argue that lower taxes are justified by differences in access to publicly funded benefits. It is true that transfers from government can favour one legal form over another. But, in practice, the differences in benefit entitlements are too small to justify anything like the scale of current tax differences. Notably, the self-employed now accrue rights to the same single-tier pension as employees.

The only publicly funded benefits to which employees are entitled that the self-employed are not, are contribution-based jobseeker’s allowance and statutory maternity and paternity pay. These can be important for the individuals receiving them, but the total revenue saving from not offering them to the self-employed is tiny compared with the £4bn of revenue foregone by charging lower National Insurance on self-employment.

One can also make a principled argument that the government may want to encourage entrepreneurship if the benefits of such activity spread beyond the individual to the wider society. But providing across-the-board tax breaks for all business owners is a very poorly targeted way of doing this. Further, any benefits must be weighed against the costs, including inefficiencies, created by having sharp tax differences across legal forms.

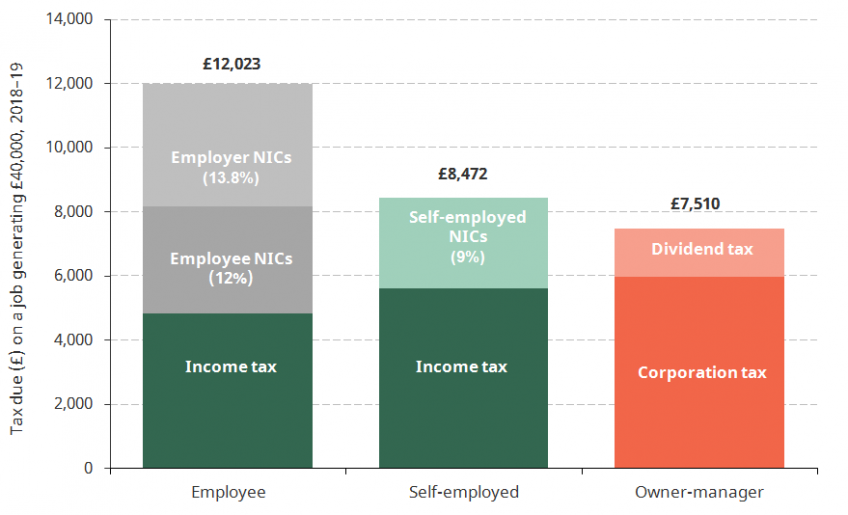

Figure 1: Tax penalty of employment

Notes: Income tax higher for the self-employed because the latter are charged income tax on income net of Employer NICs.

Tax penalty of employment shows the scale of the tax differences across different legal forms. To create a level playing field, taxes would have to be adjusted so that the overall sum paid on self-employed income was the same as that paid on employment income, including employer’s National Insurance. A well-designed system would also need

changes to the tax base to ensure that all investment costs could be deducted from taxable income. At this stage, a common objection is that employer’s National Insurance is different because it is a tax on employers, so work done through self-employment should not attract an equivalent.

This is a red herring. If employers bear this cost it gives them a reason to favour contracting with the self-employed over employees. If the cost is passed to employees through lower wages, it might prompt some to start their own business. Regardless of who hands tax to the government and how wages adjust in response, employer’s National Insurance clearly results in a system that favours operating through self-employment.

The Tax penalty of employment figure might be considered unrealistic in that it isolates the effect of income taxes on the choice of legal form to the exclusion of many real world features. It imagines a job that generates £40,000, for example the building of an extension for which a customer pays £40,000 for labour, and asks how the legal form of the person doing the job affects the total tax paid. If an employee builds the extension, the employer pays employer’s National Insurance before the employee’s income is subject to income tax and employee National Insurance. If a self-employed person does the same job there is no employer’s National Insurance, so the income flowing to the individual is higher and the overall take-home income is higher than for the employee.

Of course, one can construct more complex examples. Perhaps an employee would receive only £30,000 to build the extension because the employer had to cover the cost of administration, holiday pay and insurance. If the employer decided to contract with a self-employed trader it would be willing to pay a higher wage because it would not be covering these costs. Perhaps the employee works for a company subject to VAT while the independent business owner is below the VAT threshold; perhaps customers are willing to pay more if the work is done by a company than an independent trader; perhaps...

All of these factors will affect the work done and by whom. But to construct complex examples and use them to analyse the effect of the tax system is to compare apples with apple and blackberry crumble and custard. The figure can isolate what would happen if employer’s National Insurance were scrapped while all other factors were unchanged. One would expect employment to become relatively more attractive relative to self-employment. This is the sense in which the bar chart demonstrates the bias in our tax system.

Where to go from here?

Tax differences across legal forms bias the labour market away from employment and towards self-employment. This may not sound problematic – after all, employment is at a record high. But, as well as causing complexity and unfairness when two similar individuals receive different post-tax incomes, it leaves us with more work being carried out through self-employment than if there were no tax distortions.

We are used to celebrating all self-employment as a flourishing of entrepreneurial spirit. But discussions have highlighted that tax can drive work to be restructured in ways that make it more precarious and give workers fewer rights.

There are important debates to be had about which types of workers should have access to which rights and how the government can protect those with the least bargaining power. But that has nothing to do with how much tax someone should pay. Aligning employment rights and taxes would mean that an extension of protections to the most vulnerable workers would bring with it an increase in taxes. It would be better to remove the distortions altogether.

The Taylor Review also came to the conclusion that ‘treating different forms of employment more equally in the tax system would be fairer, more economically efficient and support better quality work’.

If we want to keep lower taxes on self-employment, a more careful discussion about what justifies such treatment is needed. I have argued that there are no credible justifications for the scale of current differences. If there is a desire to boost entrepreneurship, we should be specific about who counts as an entrepreneur and which behaviours we want taxes to encourage. We could then design better-targeted policies with fewer unintended side effects. Similarly, to help the low-income self-employed, we should look beyond blanket tax breaks and consider more targeted measures and other parts of the system including universal credit.

Levelling the tax playing field for different ways of working would require large changes – and not just for the self-employed: any rise in tax for them would increase the incentive to incorporate.

We cannot fix our tax system overnight. But it would be a great first step to acknowledge that our current system is a problem.

Authors

Helen Miller

Helen is Deputy Director of the IFS and Head of the Tax sector.

More from IFS

Understand this issue

Policy analysis

Academic research