Downloads

BN241.pdf

PDF | 744.84 KB

English local government finance is part way through a series of major changes that will see its focus shift from being based on redistribution according to spending needs, towards more emphasis on providing financial incentives to tackle needs and increase local revenue-raising capacity. In this context, the government is undertaking a ‘Fair Funding Review’. This is aimed at designing a new system for allocating funding between councils.

In particular, the Review will update and improve methods for estimating councils’ differing abilities to raise revenues and their differing spending needs. The government is looking for the new system to be simple and transparent, but at the same time robust and evidence based.

This paper focuses on the measurement of revenue-raising capacity, and discusses options for the overall design of the new funding system. A companion paper looks at the assessment of spending needs. Read a combined Executive Summary of both papers here.

How should council tax revenue-raising capacity be measured?

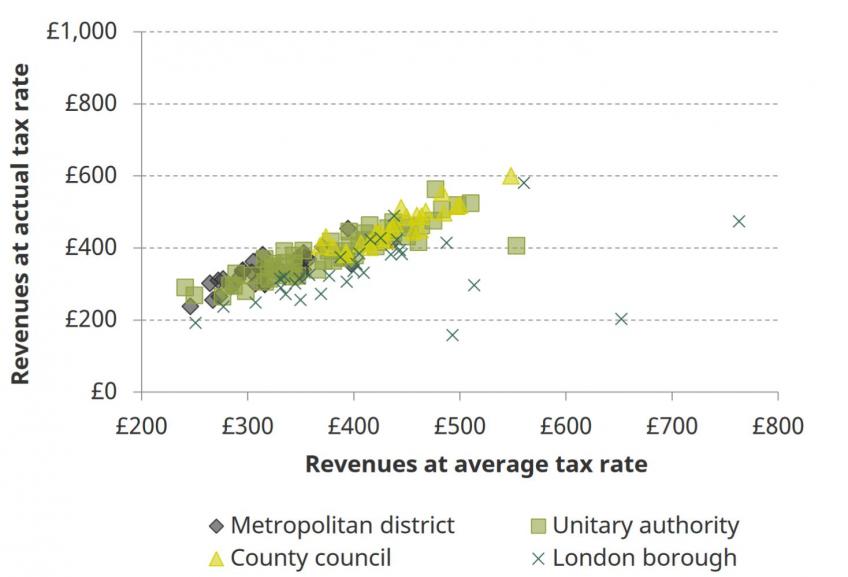

- Just over half of councils’ core spending in England is paid for from council tax. Any method for distributing funding to individual councils needs to take some account of the significant differences between councils regarding the amount of council tax they can, or do, raise. Not to do so would result in very large differences in available resources.

- However, simply taking account of current tax revenues would be inappropriate. Councils choosing to set low tax rates would be compensated via bigger grants or transfers from other councils. It could also undermine council tax as a revenue source if councils respond by cutting tax rates.

- Funding should instead depend on how much councils would raise if they all set the same council tax rate. Councils setting higher or lower tax rates would therefore retain any extra revenues or bear any cost in full.

Is a new approach needed to take account of differences in sales, fees and charges income?

- Councils also raise significant sums of money – almost £10 billion in 2016–17 – from levying various fees and charges. The amounts raised vary dramatically around the country.

- However, there is no well-defined measure of revenue-raising capacity for this income. Taking account of actual income would incentivise councils to reduce income from this source. Using statistical techniques to infer capacity from observed patterns of income would be preferable.

- Currently, income from SFCs is accounted for by using a measure of net (rather than gross) expenditure in spending needs assessments. This means it is only possible to account for differences in SFCs income to the extent to which they vary in line with the local characteristics included in the needs assessments. There could thus be benefits from including characteristics that reflect capacity to raise revenues from SFCs in the spending needs assessments.

The overall system: redistribution, incentives and transparency

- The current local government finance system is in need of change – funding depends on spending needs assessments that have not been updated for five years, and takes into account actual council tax revenues from 2015–16.

- Perhaps the most important decision that will need to be taken is what balance the new system will strike between redistributing funding between councils and providing incentives for councils to improve their socio-economic situation. The new system should allow for flexibility in the balance between the two as preferences may differ between governments and over time.

- At the same time, the system should avoid the complexity and opacity of the last system to provide such flexibility – the Four Block model in place between 2006–07 and 2013–14. The approaches in place between 1990–91 and 2006–07 provide a better starting point as they are more explicit about the role of assessments of spending needs and revenue-raising capacities in final funding allocations.

- If grant funding is retained or re-introduced at some point, which seems likely given growing spending pressures, it will not be possible to offset the same proportion of the differences between assessed relative spending needs and revenue-raising capacities for all councils unless that proportion was 100% (i.e. full equalisation of relative needs and revenue-raising capacity).

- However, it would be possible to do a full initial equalisation and then equalise the same percentage of subsequent changes in assessed needs and revenue-raising capacity for each council. And it is the treatment of these changes that is what matters for councils’ financial incentives. In particular, councils still have an incentive to tackle needs and boost revenues even if there is a full initial equalisation, provided that thereafter they retain at least some of the benefits (or bear some of the costs) of subsequent changes in spending needs and revenue-raising capacity.

Figure. Council tax revenues per person at average and actual rates, 2016-17

Authors

David Phillips

David is Head of Devolved and Local Government Finance. He also works on tax in developing countries as part of our TaxDev centre.

Neil Amin Smith

More from IFS

Understand this issue

Policy analysis

Academic research