Downloads

WP201814.pdf

PDF | 1.62 MB

This paper investigates individuals’ expectations about their own survival to older ages and compares these to projected and actual survival rates. The extent to which individuals have, on average, reasonable expectations about survival to older ages is important in a context of increasing personal responsibility for, and control over, the accumulation and use of retirement savings.

We use data from the English Longitudinal Study of Ageing, which surveyed a representative sample of the English household population aged 50 and over between 2002–03 and 2014–15, and the ONS 2014-based life tables for England and Wales.

Subjective expectations of survival

- Modern surveys ask individuals about their probability of survival to specific older ages. In only a small proportion of cases is there clear evidence that these questions are not understood. 98% of individuals gave an answer to a question asking their chances of surviving to older ages and of these just 14% – i.e. fewer than one-in-six – showed clear evidence of misunderstanding (e.g. by reporting no chance of death in the coming 10-year period).

- Individuals’ stated beliefs about their probability of survival are correlated with known risk factors such as smoking and the age that their parents died. Those who currently smoke report on average 6–8 percentage points lower chance of surviving to an age 11–15 years ahead than do people who have never smoked. Those whose mother died at age 85 or older report on average 5-7 percentage points higher chance of surviving to an age 11–15 years ahead than do those whose mother died aged 60-64.

- Beliefs about probability of survival are also correlated with the individual’s actual age of death and respond to new diagnoses of health conditions. Those reporting a 10% or less chance of survival to an age 11–15 years ahead were more than twice as likely to die in the following 10 years than those who reported a 50% or greater chance of survival. A new cancer diagnosis was associated with a 5 percentage point reduction in the stated probability of surviving to an age 11–15 years ahead.

Comparing subjective expectations with life table estimates and mortality data

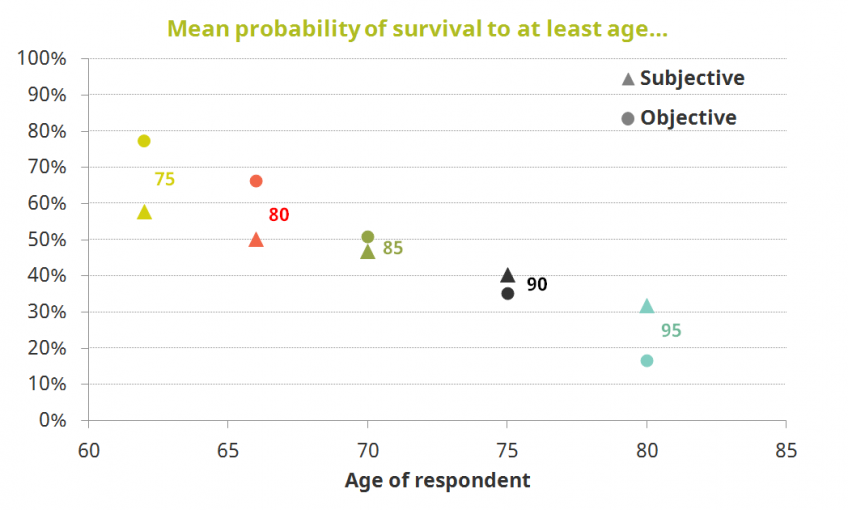

- Relative to life tables, individuals from a range of ages and birth cohorts underestimate their chances of survival to ages 75, 80 and 85, on average. Those in their 50s and 60s underestimate their chances of survival to age 75 by around 20 percentage points and to 85 by around 5 to 10 percentage For example, men born in the 1940s who were interviewed at age 65 reported a 65% chance of making it to age 75, whereas the official estimate was 83%. For women, the equivalent figures were 65% and 89%.

- Individuals in their late 70s and 80s are, on average, optimistic about surviving to ages 90, 95 and above. This optimism becomes larger at older ages (10–15 percentage points when looking at age 95) and is larger for men than for women, amongst those born in the 1920s and 1930 For example, men born in the 1930s who were interviewed at age 80 reported a 32% chance of making it to age 95, whereas the official estimate was 17%. For women, the equivalent figures were 37% and 24%.

Figure 1.1. Comparing subjective reports and “objective” life table estimates of survival probabilities (for men born 1930-39)

Note: Different coloured series correspond to different ages about which respondents are asked questions. Source: ELSA waves 1–7 and ONS 2014-based cohort life tables for England and Wales.

- Subjective survival curves, estimated using individuals’ stated survival expectations, capture the general patterns in expectations. These show growing pessimism relative to official life tables for ages up to the mid 70s before turning to optimism from the late 90s onwards.

- Actual survival probabilities differ significantly according to individuals’ education, wealth and marital status. Women aged 60 in the bottom household wealth quintile had a 65% chance of surviving to age 80, compared with 87% for those in the top quintile, based on actual mortality data.

- Subjective survival curves reflect differences in actual mortality rates between groups to varying degrees. Widows and widowers aged 60 show the greatest survival pessimism. While their estimated chances of surviving to age 80 were 77% and 67%, respectively, their subjective survival curves implied a 49% and 39% chance, respectively, a gap of almost 30 percentage points in both cases.

Subjective expectations and economic behaviour

- Survival pessimism is a potential driver of the unpopularity of annuities. An annuity priced according to average survival chances should represent a fair deal (or better) for around half of individuals. But given individuals own survival expectations, around two-thirds of individuals in their 60s would perceive an annuity priced according to average survival chances as offering a less than fair deal.

- Deferral of the state pension, a choice analogous to annuity purchase, is rarely taken up despite being offered at a favourable rate. While individuals are roughly twice as likely to defer the state pension if it represents a ‘fair deal’ given their survival expectations, the overall level of deferral is sufficiently low that we cannot make strong statements about this relationship.

- Optimism about survival at the very oldest ages may lead to reluctance to spend remaining wealth if an individual survives through their 80s and into their 90s or beyond.

As individuals are given more control over saving for retirement and use of accumulated wealth, the divergence between subjective expectations and official projections of survival is a concern.

- Survival pessimism may mean that individuals save less during working life, and spend more in the earlier years of retirement, than they would, given their actual survival chances.

- The risk of this faster-than-optimal spending down of wealth, combined with optimism about survival at the very oldest ages, means that if individuals survive through their 80s and into their 90s, they may not only have relatively low levels of wealth, but may then be reluctant to spend this, with negative consequences for their living standards.

Authors

Cormac O'Dea

Cormac is a Research Associate of the IFS, an Assistant Professor of Economics at the Yale University and Research Fellow at the NBER.

David Sturrock

David’s research covers household wealth, intergenerational transfers, social mobility, pensions taxation, and health and work at older ages.

More from IFS

Understand this issue

Policy analysis

Academic research