From tomorrow, a large proportion of private sector employees will pay more into their pensions – and their employers will have to contribute more too. This is the first of two planned steps in the next two years that will increase the minimum contributions that most employees and their employers will, by default, make to a workplace pension. This is all part of the government’s automatic enrolment policy aimed at increasing retirement saving.

In this observation, we summarise the changes that are coming in tomorrow and discuss what effect they may have on employees and their pensions.

Automatic enrolment so far

Automatic enrolment is a flagship government pensions policy that means that all eligible employees must be enrolled into a workplace pensions scheme (a pension scheme arranged by their employers). Until tomorrow the minimum default contributions that must be made were 2% of “qualifying” earnings (between £5,876 and £45,000 in 2017–18), of which at least 1% must come from the employer. The employee can choose to “opt out” and leave the pension scheme (in which case both they and their employer will stop contributing), but unless the employee actively does this, they will remain part of the scheme.

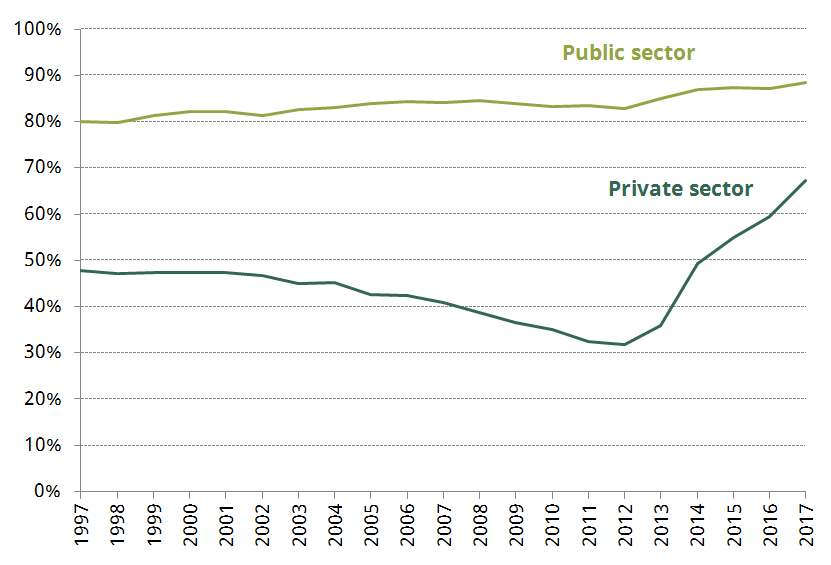

This policy has been gradually rolled out since the Autumn of 2012, starting with the very largest employers and progressively including smaller and smaller employers. Employees are eligible if they earn the equivalent of at least £10,000 per year, are aged between 22 and the state pension age, and have worked at their employer for at least 3 months. The policy has led to an enormous increase in the proportion of private sector employees who are saving for their retirement in a workplace pension. As shown in Figure 1, it doubled between April 2012 and April 2018, rising from one-third (32%) to two-thirds (67%). This increase has reversed the decline in private pension membership seen since the 2000s, and leaves membership much higher than the levels seen in the late 1990s (it was 48% in 1997), though it is still lower than the levels seen in the public sector. Previous IFS research has shown that the increase since 2012 has been directly driven by the introduction of automatic enrolment.

Figure 1: Workplace pension membership rates among public and private sector employees, 1997 to 2017

Source: ONS ASHE Pension Tables (2011 to 2017) and Cribb and Emmerson (2016) calculations using ASHE microdata (1997 to 2010).

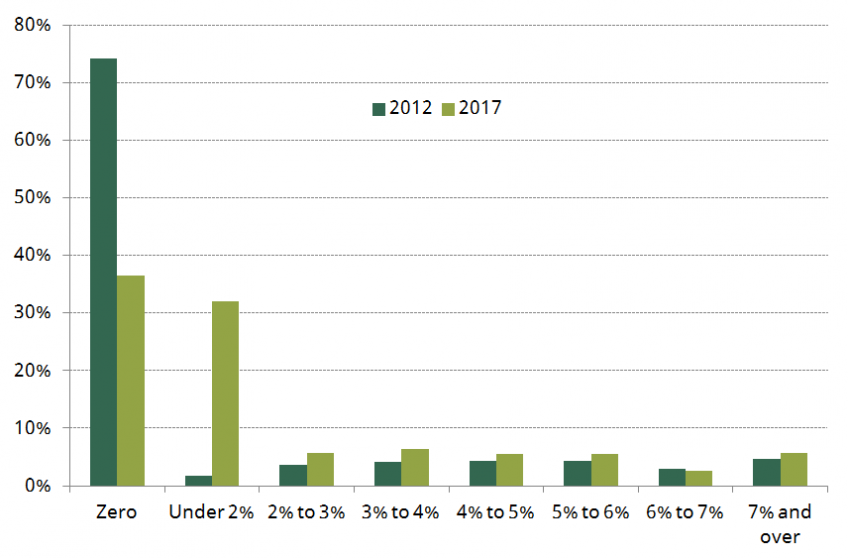

Although pension membership has risen enormously, the number saving large proportions of their earnings has not. Automatic enrolment has mainly increased the proportion of employees and employers making very low contributions at the minimum levels. Figure 2 shows a very large increase in the proportion of employees who are in a workplace pension but who are contributing less than 2% of their earnings since 2012 – increasing from just 2% to 32% of private sector employees. It is a similar story with employer contributions. Therefore, although many more people are contributing to a pension, it is, in most cases, only at very low levels. There is however a slight increase in the proportion of employees who are making more significant contributions: in 2012 5% of private sector employees were making an employee contribution of more than 7% to a workplace pension; by 2017 this figure had increased to 6%.

Figure 2: Distribution of employee contribution rates for all private sector employees in 2012 and 2017.

Source: Authors’ calculations using ONS ASHE Pensions Tables 2012 and 2017.

Increases in minimum default contributions happening tomorrow

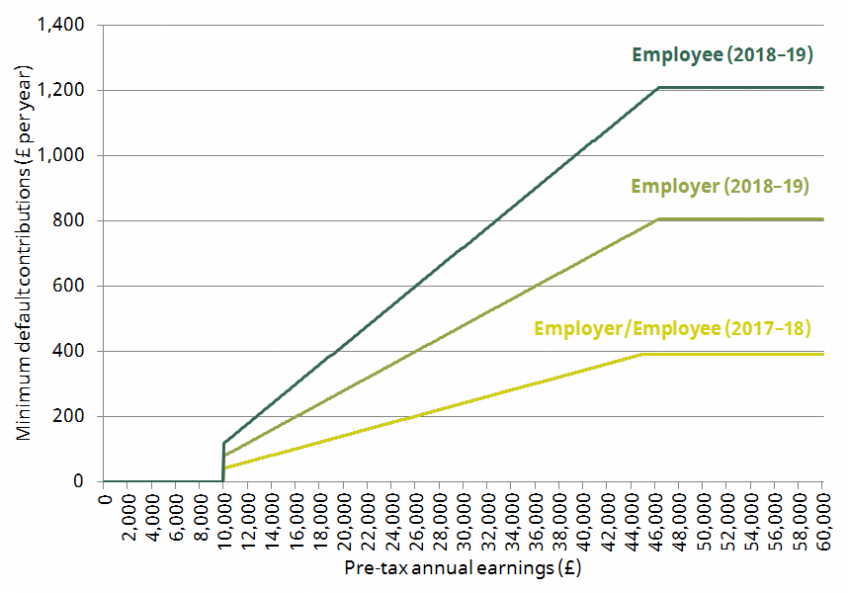

The changes happening tomorrow are aimed at increasing the amounts saved in workplace pensions. Currently, the minimum default rate that can be contributed is 2% of “qualifying earnings”, with at least 1% coming from the employer. Tomorrow, the minimum default rate will more than double to 5% of “qualifying earnings” (£6,032 to £46,350 in 2018–19), of which at least 2% will come from the employer. In April next year, the minimum contributions will rise again, to 8% of qualifying earnings, with at least 3% coming from the employer.

Figure 3 shows how much these minimum contribution rates amount to, in 2017–18 and in 2018–19, for people earning between £0 and £60,000 per year. An employee earning £10,000 per year who currently makes and receives minimum contributions will see an increase of at least £38 per year in their employer contribution (from £41 per year to £79 per year), and will make an additional £78 per year of employee contribution (from £79 per year to £119 per year). The maximum increase is for someone earning £46,400 or more, who will receive an additional £415 per year (from £391 per year to £806 per year) from their employer, and make an additional employee contribution of £818 per year (from £391 per year to £1,210 per year).

Of course, while the higher employer contributions will reduce take home pay for employees, they will not reduce it by as much as suggested here. Since contributions to pensions are exempt from up-front income tax, employees will pay lower income tax as a result of higher contributions (worth at least 20% of the contribution for those who pay income tax in 2018–19) – though of course income tax is likely to be paid when the pension is drawn). Furthermore, if they contribute through a “salary sacrifice” arrangement – they will not pay any NICs on the contributions either (either when the contribution is made or when the pension is drawn).

Figure 3: Minimum default employee and employer contributions to workplace pensions in 2017–18 and 2018–19 (£ per year)

How will people respond?

Importantly, a significant number of private sector employees will not be directly affected by tomorrow’s changes. At least 28% of private sector workers in 2017 are already in a scheme with higher default employer contributions than the total minimum default mandated by the government. A further 32% are not in a workplace pension scheme – either because they have not been enrolled automatically (for example if they earn below £10,000 a year then their employer does not have to enrol them automatically) or because they chose to opt out after being enrolled – , and so are not affected by the rising contributions either.

However, the change will still be a hurdle for the government’s automatic enrolment policy. So far, the proportion of employees choosing to leave their workplace pension after having been enrolled automatically has been small. It is an open question whether employees will continue to stay in their workplace pension schemes, and whether newly enrolled employees stay in at the same rate, or whether more will choose to opt out because of higher required contributions.

There are at least three theoretical reasons to for the government to be optimistic that the proportion of people opting out will not increase markedly. First, individuals procrastinate when making saving decisions and tend to shy away from making complex choices. This means that when they are defaulted into a workplace pension some will remain in the scheme simply due to inertia. Second, individuals would be giving up a (now larger) employer contribution if they chose to opt out, which gives them a financial incentive to remain in their pension. Third, it is possible that the default minimum rates are seen as being endorsed – perhaps by their employer, or by the government, or perhaps even by their colleagues who are remaining in the scheme – and therefore employees will choose to remain in their pension with the higher rate of contributions. Furthermore, there is evidence from the United States, where companies have introduced automatic enrolment with higher default contributions, that suggests that coverage rates may hold up: Madrian and Shea (2001) studied a firm which had default rates of 3% from employer and 3% from the employee, and found that only 14% of workers opted-out (not that much higher than among large firms in the UK while default total contributions have been at 2%).

Pension membership rates going forwards therefore need to be carefully monitored. But a harder, and arguably more important question, is where the additional pension saving of those who stay in their pensions at higher default contribution rates is coming from. If employees are saving an extra 2% of “qualifying earnings” in their pension, are they spending less (and if so, on what) or are they saving less in other forms? That is what will matter for the government’s ultimate ambition of increasing individuals’ retirement resources – increasing workplace pension coverage and pension savings is a means to an end, rather than the end itself.

Authors

Carl Emmerson

Carl, a Deputy Director, is an editor of the IFS Green Budget, is expert on the UK pension system and sits on the Social Security Advisory Committee.

Rowena Crawford

Jonathan Cribb

Jonathan is an Associate Director and Head of Retirement, Savings and Ageing sector, focusing on pensions, savings and later-life economic activity.

More from IFS

Understand this issue

Policy analysis

Academic research