These remarks were written for the IFS Autumn 2017 post-Budget briefing.

Yesterday’s Budget was more about the OBR’s forecasts than it was the Chancellor’s policy decisions. The forecasts for productivity, earnings and economic growth make pretty grim reading. One should never forget of course that these are just forecasts. But they now suggest that GDP per capita will be 3.5% smaller in 2021 than forecast less than two years ago in March 2016. That’s a loss of £65 billion to the economy. Average earnings look like they will be nearly £1,400 a year lower than forecast back then, still below their 2008 level. We are in danger of losing not just one but getting on for two decades of earnings growth.

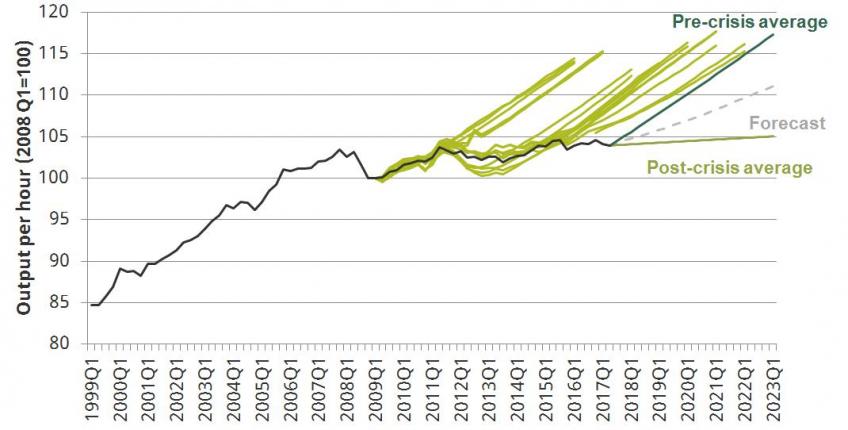

OBR now more pessimistic about productivity: successive forecasts for productivity growth

Source: OBR Economic and Fiscal Outlook November 2017

The knock on effects on forecast borrowing are obvious – it will be pushed up. The Chancellor was spared maximum embarrassment by better than expected borrowing numbers this year and a rather handy £5 billion resulting from a reclassification of Housing Associations and other ONS changes. Even so, before any policy changes, borrowing is now forecast to be £12 billion higher in 2021–22 than was forecast in March.

The response was not to turn the fiscal screws even tighter. It was not even to leave policy neutral. Rather it was to implement a giveaway peaking, for now, at £9 billion in 2019–20. Taking the figures at face value that giveaway dissipates very quickly thereafter, magically becoming a takeaway by 2022–23. Taking the figures at face value would probably be a mistake though – as the realities of 2022–23 hove into view the purse strings are likely to be loosened once again. As the OBR notes there is an Augustinian tinge to these plans “Lord make me pure, but not yet”.

Less than two years after Mr Osborne was promising a surplus of £10 billion in 2019–20 Mr Hammond is promising a deficit of £35 billion falling, rather optimistically, to £25 billion by 2022–23. Note that even without any forecast revisions the 2020–21 surplus would have been wiped out by new policy measures announced since March 2016.

Yet this is not the end of “austerity”. Not by a long chalk. There are still nearly £12 billion of welfare cuts to work through the system, while day-to-day public service spending is still due to be 3.6% lower in 2022–23 than it is today. Excluding health the cut for the rest of public services is over 6% - to keep this spending constant in per capita terms spending would need to be £13 billion higher in 2022-23 than currently planned. The figures published yesterday also imply yet one more year of spending restraint. As the years go by the end of austerity keeps slipping out of view.

Forecasts

The reasons for the OBR’s downgrades are clear enough. Productivity has consistently underperformed forecasts, and by a lot, over the past seven years. It is doing so again in 2017. The OBR judged that the time had come to assume that things would not bounce back close to the pre-crisis normal any time soon. They now expect productivity to grow at around 1% a year for the next few years rather than 1.7% which they expected back in March. Given that the post-crisis average has been an increase of more like 0.3% a year it is hard to argue that this is unduly pessimistic. It is of course a judgment call. It looks about as likely to be too optimistic as to be too pessimistic, which is exactly what it should be.

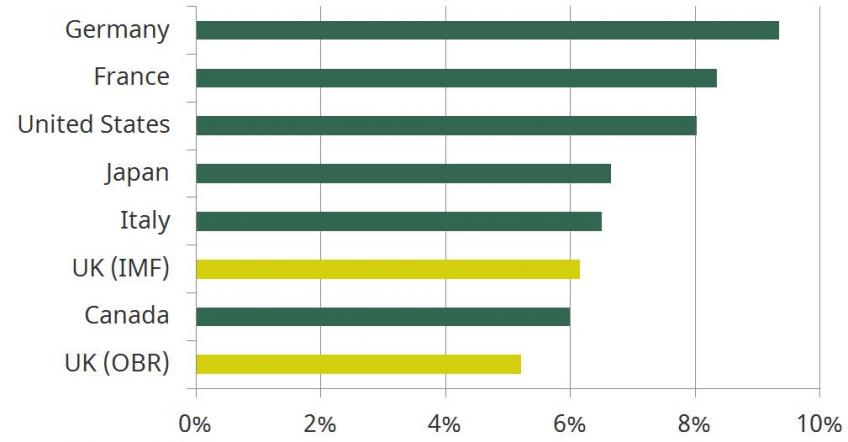

In response to weaker earnings the OBR expects some to work more hours. And they have also revised up their forecasts of employment. But overall this still this leaves growth forecasts down, and reaching a maximum of just 1.6% a year by the end of the forecast period. It really is time to start forgetting that for decades anything less than 2% was considered seriously disappointing. Compare OBR forecasts with IMF forecasts for the other G7 economies and the UK comes out well behind all of them with only Canada even within touching distance. And we don’t have to rely just on forecasts. The UK is currently growing more slowly than other advanced economies.

OBR expects UK to perform worse than main competitors: forecast cumulative real GDP per capita growth in the G7, 2016–2022

Source: IMF World Economic Outlooks Database, October 2017 and OBR EFO November 2017

The immediate effects of all this on households is already being felt. Real earnings are falling this year as inflation has risen to 3%. The nascent recovery in earnings, which were growing through 2014 to the first half of 2016, has been choked off. That they even might still be below their 2008 level in 2022 as the OBR forecasts is truly astonishing. Let’s hope this forecast turns out to be too pessimistic.

Fiscal

Of course slower growth means higher borrowing. Taking account of policy change as well as forecast changes borrowing in 2019–20 is now expected to be £35 billion, falling to £33, £30 and £26 billion over the following years. All those numbers would be £5 or 6 billion higher if they weren’t being flattered by classification changes. And we are likely to see extra spending unveiled for the later years pushing the deficit up further.

We are still on course to meet the 2020 target for borrowing to be less than 2% of national income, though with rather less headroom than before. The chances of getting to budget balance by the mid 2020s look remote.

To be fair to the government it has been open and transparent about how it has treated the public finance rules. Regarding changes to the regulations surrounding housing associations they stated “The only reason these regulations have been introduced is to seek ONS to reclassify housing associations to the private sector”. As the OBR observe “It is hard to argue that the change in statistical treatment reduces the de facto exposure of the government to these organisations”. It’s always important to look behind the headline numbers.

Does any of that matter? Well austerity is continuing to bite, interest rates remain extremely low, and debt remains on course to start falling as a fraction of national income. There are arguments for more borrowing.

The trouble with lower projected growth rates though is that they imply debt being higher over time for any given level of borrowing. Debt fell rapidly after the second world war whilst we still ran modest deficits because nominal growth was strong. The sorts of modest growth rates currently expected imply that, if we were to maintain the deficit at the just over 1% of national income projected for the early 2020s, it would take us until well past 2060s for debt to fall to its pre-crisis levels of 40% of national income. That assumes no recessions for the next half century.

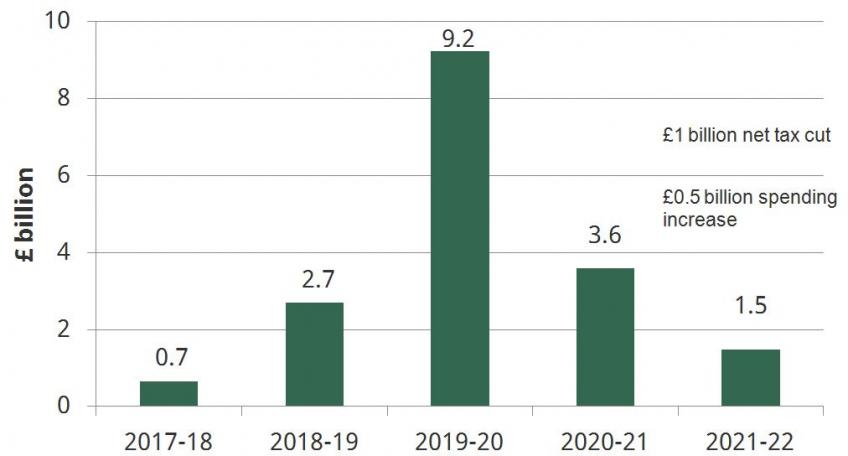

Policy measures increase medium term deficit: effect of announced policy changes, Autumn Budget 2017

Source: OBR Economic and Fiscal Outlook November 2017

Spending

There were some giveaways yesterday but the wider fact remains that most areas of public spending still have difficult years ahead. Day to day spending on public services outside of the NHS is due to fall by yet another 7% over the next five years. In truth I would be amazed if that actually happened. The last few years have been marked by constant (small) upgrades to implausibly tight spending plans to avoid problems in prisons, social care and now health. There will almost inevitably be more such top ups in the years ahead.

The planned increases in health spending remain modest in the context of easily the tightest decade for the NHS since its founding. Changes to Universal Credit, while helping with one particular problem, are also modest costing just £300 million a year in the context of planned working age benefit cuts of nearly £12 billion. But they are well targeted at those who find it difficult to cope with the six week wait before their Universal Credit comes through.

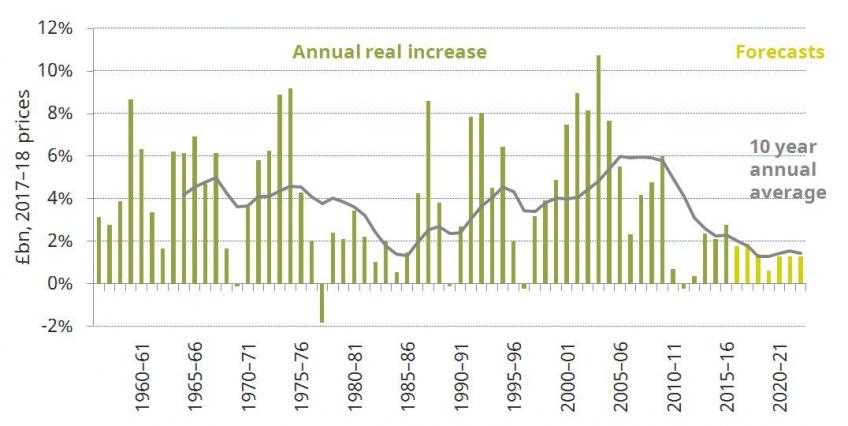

Still consistently the toughest decade for the NHS

Source: Author’s calculations using Office of Health Economics, HMT PESA 2017, Autumn Budget 2017, OBR Nov 2017 EFO.

While the public pay cap has been lifted no additional money has yet been allocated and the Treasury is committed to providing extra money only for nurses. Given the spending constraints, other public sector workers should not be holding their breath in anticipation of an inflation busting, or perhaps even 1% busting, pay rise.

One form of spending where Mr Hammond has been quite generous is investment spending. He topped up plans last year and again this such that public sector investment is due to rise towards 2.4% of national income. This would be, if sustained, its highest level in 40 years. Given the more immediate pressures on spending this is a brave focus on the long term, one which previous chancellors have always shied away from, especially when money has been tight. Hopefully it will pay off.

Investment planned to increase to levels not sustained in 40 years

Source: Office for Budget Responsibility.

Housing

Whilst putting housing at the centre of his Budget Mr Hammond didn’t actually commit a lot of additional public spending to building houses. You’d be forgiven for thinking that he had. “Over the next five years we will commit a total of at least £44 billion of capital funding, loans and guarantees to support our housing market” is how he put it in his speech. That translates into about £1.5 billion a year of actual public spending.

That’s not to say that the overall plan – with additional guarantees for Housing Associations, borrowing powers for local authorities, money for infrastructure and a review of planning – is not sensible. Their actual impact though remains to be seen.

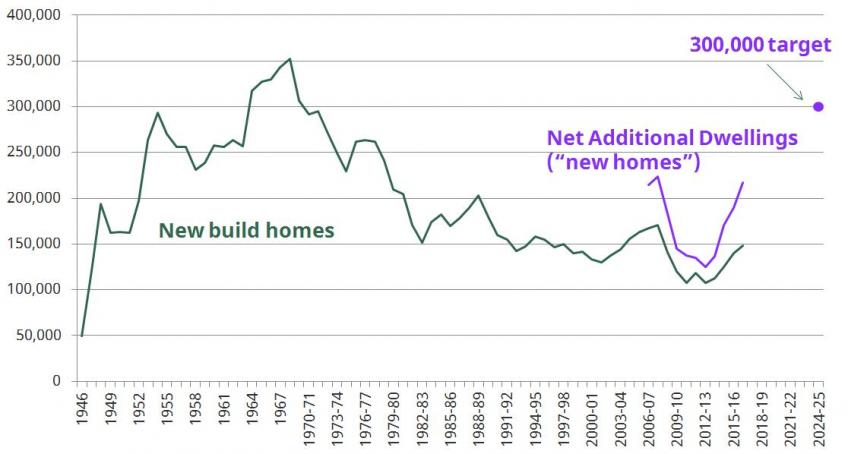

300,000 in historical context: a big number: new homes over time (England only)

Source: DCLG Live Tables 244 and 120

Suppose we do get 300,000 new homes a year. Might that reverse the fall in home ownership among the younger generation? It’s important to think clearly here. That fall up to now is not because young people are living nowhere, it’s because they are renting from older people who have bought properties to rent out because that provides a good return. Older, richer people might continue to buy these new properties. They will stop doing so only when they take the view that the return in terms of rent and capital gain is not worth their while – the consumption value of housing needs to rise relative to its investment value. That’s how the actuality and promise of more house building can tip the scales in favour of younger buyers.

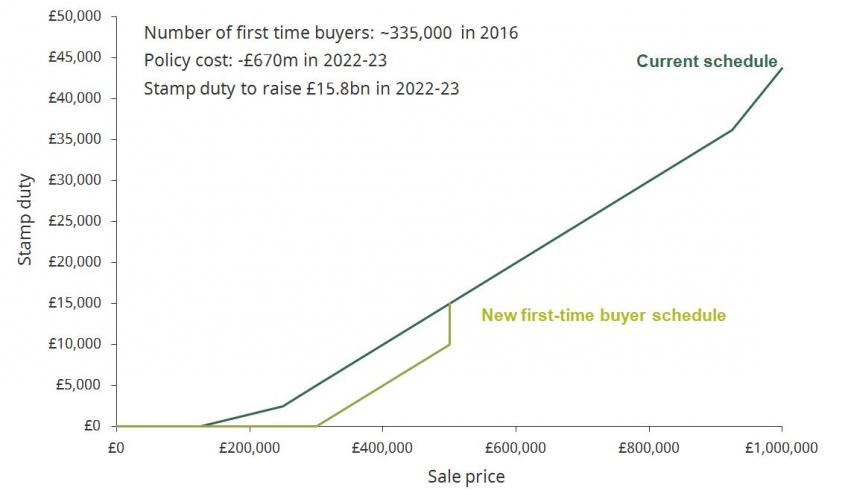

It’s also important to think clearly about the impact of stamp duty. The OBR has said that the price faced by first time buyers might rise twice as much as the saving in stamp duty. Stamp duty cuts do lead to price rises. The price rise can be bigger than the duty cut in part because properties are transacted multiple times and in part because of the leverage effect – if I pay £1 less in stamp duty I can put down £1 more deposit, meaning I can obtain a larger mortgage. So the £1 cut allows me to spend more than £1 more on a house.

But this does not mean first time buyers are worse off as a result. They are in general better off. Instead of paying, say, £100,000 for £98,000 worth of house plus £2,000 of tax they might be paying £102,000 for £102,000 worth of house. That’s a better outcome for them.

Stamp duty change

And finally

I’ve got to here without mentioning the B word. Where is Brexit in all of this? Of course there is the £3 billion set aside for preparations over the next two years. There is no mention of a divorce payment.

As far as the economic forecasts as concerned the OBR rather plaintively says “we asked the government whether it wished to provide any additional information on its current policies in respect of Brexit that would be relevant to our forecasts. It directed us to the prime minister’s Florence speech from September and a white paper on trade policy published in February…

Given the uncertainty regarding how the government will respond to the choices and trade-offs it faces during the negotiations, we still have no meaningful basis on which to form a judgment as to the final outcome and upon which we can the condition our forecast”

So the economic impact wrapped up in their forecasts is the same as they made a year ago based on what they describe as some fairly “broad brush” assumptions. Just to recap on what the OBR said a year ago. Their view then, accepted by government, was that the Brexit vote would result in a £15 billion a year deterioration in the public finances. They have not changed that judgment. The additional slow down in this year’s forecasts are not put down to Brexit.

So despite all this focus on the forecasts the overwhelming fact of pervasive economic uncertainty remains. Despite all the gloom we can hope for better – though we may still fear for worse. Or in the words of Benjamin Disraeli we should perhaps “be prepared for the worst, but hope for the best”.

Authors

Paul Johnson

Paul has been the Director of the IFS since 2011. He is also currently visiting professor in the Department of Economics at University College London.

More from IFS

Understand this issue

Policy analysis

Academic research