In the Autumn Statement last week, the Chancellor announced a new government-backed loan scheme for postgraduates. Loans of up to £10,000 are to be made available for under-30s studying full-time or part-time for taught masters courses from 2016/17. The government expects 92,000 people to be eligible for the loans in the first year they are available, and intends the long-run cost of the scheme to be zero, meaning that the full value of loans will be repaid, on average. While full details of the loan system have yet to be announced – and will be subject to consultation – the documentation accompanying the Autumn Statement highlighted one way in which the scheme could operate. This observation assesses the example loan scheme put forward and raises some issues that should be considered during the consultation.

The loan system announced by the Chancellor should help individuals who may otherwise be prevented from continuing into postgraduate study because they are credit constrained. If the value of the loans issued were not repaid in full, then it would also represent a government subsidy for postgraduate education, just as there is in the undergraduate student loan system. (Previous IFS research estimated that the government can only expect to recoup 57% of the value of undergraduate student loans, representing a considerable government subsidy.) However, the Autumn Statement made clear that the government intends the loans issued to postgraduates to be repaid in full, on average, suggesting that it does not wish to subsidise loans for postgraduate study.

In the illustrative scheme put forward in the Autumn Statement loans of up to £10,000 will be made available to those under the age of 30 studying for taught masters courses. English students studying in the UK and EU students studying in England would be eligible. The loans will be subject to a real interest rate of 3% (i.e. interest will be charged at RPI plus 3%) and will be repaid at a rate of 9% of income above a lower-income threshold of £21,000, which would be frozen in nominal terms for 5 years. We assume that all other features of the repayment system follow that of the undergraduate loan system, i.e. that individuals incur an interest rate of RPI plus 3% while they are studying; that the lower earnings threshold is uprated by average earnings growth after the five year period; and that postgraduate debt will be written off after 30 years.

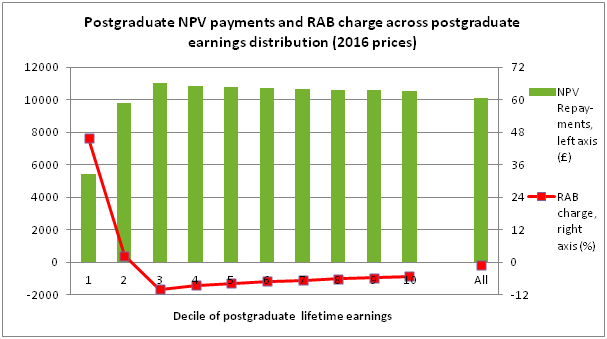

Our estimates of the future repayments that would be made under such a scheme are outlined in Figure 1. These estimates are calculated for English-domiciled students using repayments made on the basis of lifetime earnings rather than income and assume that repayments are made in line with the repayment schedule (with no under- or over-payments). We estimate that the government could expect to recoup 100% of the value of these loans in the long-run (i.e. that the so-called RAB charge – the long-run cost to the government of issuing student loans – is effectively zero).

This differs from estimates of the long-run cost of the undergraduate loan system – which we estimate will cost the government 43p for every £1 loaned out – for three reasons. First, and most importantly, postgraduates will borrow considerably less: the maximum postgraduate loan will be £10,000, while the average undergraduate loan is around £44,000. Second, according to recent estimates, postgraduates earn around £200,000 more over their lifetimes, meaning they repay more quickly. Third, the illustrative loan scheme suggests that they would be charged higher interest rates on their loans than most undergraduates.

Figure 1: Net Present Value (NPV) of postgraduate loan repayments made and RAB charge, by distribution of postgraduate lifetime earnings distribution (2016 prices)

Figure 1 also shows how repayments vary across the distribution of lifetime earnings amongst postgraduates. It shows that in all but the first decile of lifetime earnings, loans are close to being repaid in full, on average. Indeed, less than 15% of postgraduates do not repay the full value of their loan, and repayments are, on average, highest in the third decile of lifetime earnings. This relative lack of progressivity is a consequence of the positive real interest rate charged and the fact that repayments are lower than the interest accrued at relatively low earnings. Individuals higher up the earnings distribution also repay more quickly, on average, with those with the highest lifetime earnings repaying in full within seven years of graduating.

There are a number of assumptions that underlie these estimated figures, all of which introduce risk to the government that the long-run cost of issuing loans to postgraduates may turn out to be different from zero. Two important assumptions for the total cost of undergraduate loans were the long-run real earnings growth rate and the population of borrowers. However, for postgraduates these assumptions are less important, as the loan is relatively small in comparison.

For example, while changing our assumption about long-run real earnings growth from 1.1% to -1% increased the RAB charge from 43% to 52% for the undergraduate loan scheme, for postgraduates it increases only slightly, from -0.9% to 1.3%. Similarly, even if we were to assume that only the lowest earning 56% of postgraduates take out loans (this is the take-up rate assumed by the Autumn Statement), the RAB charge would still be very small: around 3%. This lack of sensitivity arises mostly because the value of the loans issued is relatively small compared to the undergraduate scheme, but is also partly driven by the features of the illustrative loan scheme. If, for example, the interest rate charged were to increase with income, then the burden of repayment would fall more heavily on higher earners, but the RAB charge would also become more sensitive to changes in the population of borrowers. This represents an important trade-off that should be considered when designing the repayments system.

One assumption to which our findings are sensitive is that of repayment compliance. In 2012/13, 13.5% of new postgraduate students in the UK were EU domiciled. If the same proportion of EU students took out loans, but the government were unable to collect any repayments from these students, we estimate that the RAB charge would increase to 12.6%. This is another important consideration for the policy consultation.

An additional concern with the introduction of the government’s illustrative example is the high marginal tax rate that individuals would face under the new system. Since repayments on the postgraduate loan would be made “concurrently” with undergraduate repayments, individuals earning between the lower loan repayment threshold (of £21,000 in 2016 prices) and the higher income tax-rate threshold would face marginal tax and employee NICs rates of 50%, while those earning above the higher rate tax threshold would face marginal rates of 60%. This could potentially affect the labour supply decisions of young postgraduates and hence may have wider consequences for growth and productivity.

It would also introduce a further complication to the tax schedule faced by postgraduates: while the repayment threshold for undergraduate loans looks set to be uprated in line with average earnings growth, the Autumn Statement documentation suggests that the repayment threshold for postgraduate loans would be frozen in nominal terms for five years (we have assumed that it would rise at the same rate as the undergraduate threshold thereafter). This would create an increasingly large range over which repayments would be due on any outstanding postgraduate loan but not on any outstanding undergraduate loan. Of course, this is just an illustrative example, and the government will consult before outlining the specifics of the policy, but it will be important to consider such features.

Ultimately, the success of the policy will be determined by the responses of both students and universities. Are credit constraints a primary driver of individuals’ decisions not to stay on for postgraduate study, and if so is the new scheme sufficient to alleviate these constraints? The response of universities is also uncertain. While the proposed postgraduate loan scheme does not link loans to fees in the same way as it does at undergraduate level, institutions with high market power might still respond to the increased availability of credit by raising prices, which would reduce the effectiveness of the policy in making the upfront costs of postgraduate study cheaper. Thus, while the introduction of a loan scheme is broadly welcome, the devil will, as always, be in the detail.

Authors

Lorraine Dearden

Claire Crawford

Claire is a Research Fellow at IFS, working on the determinants and consequences of participation in childcare and education for parents and children.

Jack Britton

Jack's main interests lie in human capital accumulation and discrete choice dynamic modelling.

More from IFS

Understand this issue

Policy analysis

Academic research